2024 401(k) and IRA Contribution Limits

Key Points – 2024 401(k) and IRA Contribution Limits

- Contribution Limits for 401(k)s, 403(b)s, 457(b)s, and Thrift Savings Plans

- IRA and Roth IRA Contribution Limits Increase for Second Straight Year

- SEP and SIMPLE Contribution Limits

- Remembering That Contribution Limits Are Tied to Inflation

- 4 Minutes to Read

2024 401(k) and IRA Contribution Limits Are Going Up Again

The IRS announced increases to 401(k) and IRA contribution limits for 2024 on November 1. Let’s review those increases, explain why they happened, and the importance of maximizing your contributions.

2024 Workplace Retirement Plan Contribution Limits

From 2022 to 2023, there was a $2,000 increase to workplace retirement plan contribution limits. Those include 401(k)s, 403(b)s, and most 457(b)s. There will be a $500 increase for those retirement plan contribution limits for 2024, as they’ll go up from $22,500 to $23,000. Federal employees with Thrift Savings Plans will see that same increase.

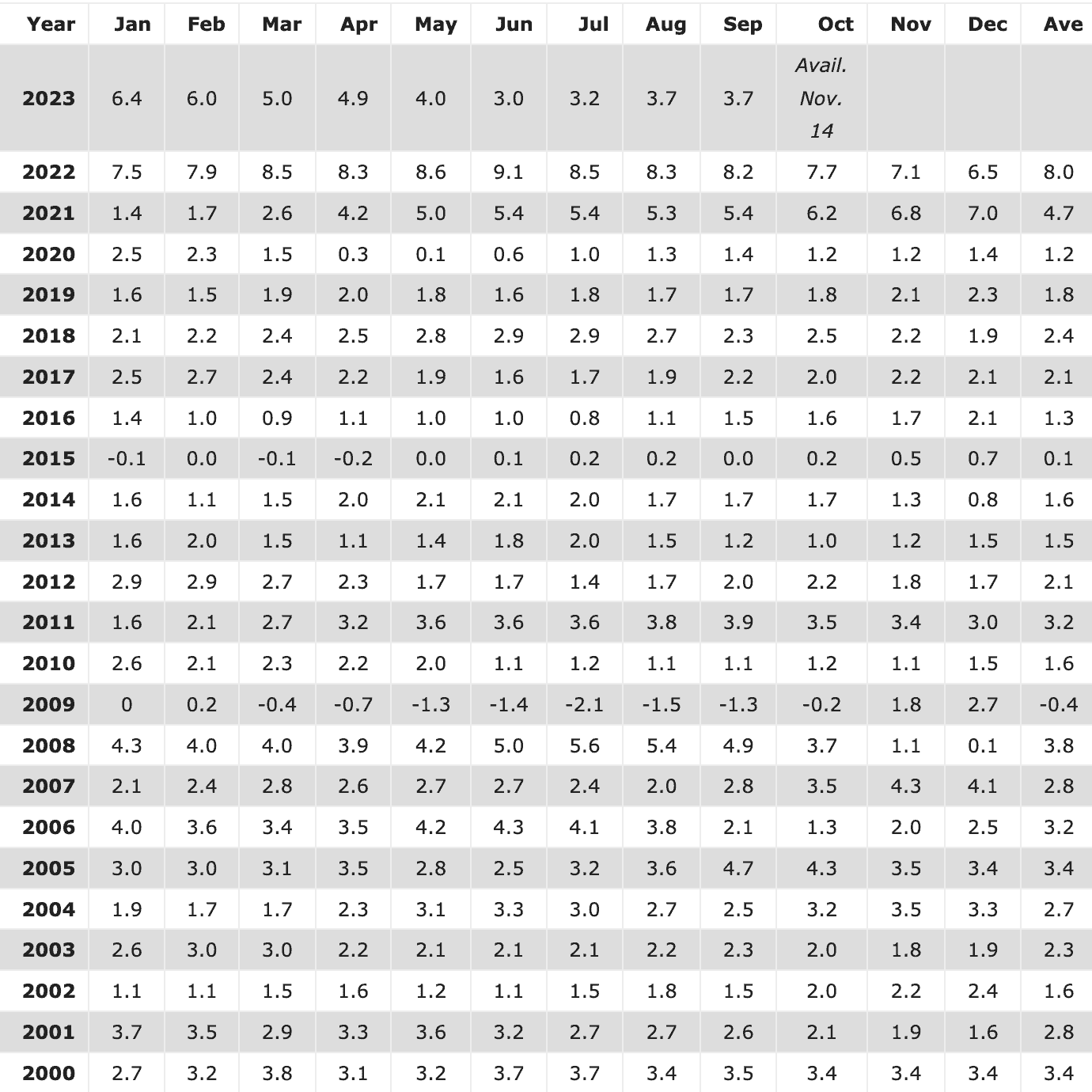

So, why was the increase so much larger in 2023 than it will be for 2024? That answer lies below in Figure 1. Retirement plan contribution limits are tied to inflation, and the U.S. inflation rate was substantially higher at this time last year than it is now.

FIGURE 1 – U.S. Inflation Month by Month – U.S. Bureau of Labor Statistics/U.S. Inflation Calculator

Don’t Forget About Catch-up Contributions

People who are 50 or older have another opportunity to take advantage of with retirement plan contribution limits. We’re talking about catch-up contributions. Those, however, aren’t tied to inflation. The catch-up contribution limit for 401(k)s, 403(b)s, most 457(b)s, and Thrift Savings Plans for 2024 is $7,500. That’s the same as it was for 2023. So, you can maximize your contribution at $30,500 in 2024 if you make a full contribution ($23,000) and catch-up provision ($7,500).

2024 Traditional and Roth IRA Contribution Limits

The contribution limits for IRAs and Roth IRAs are increasing by $500 for the second straight year, going up for $6,500 to $7,000. That $7,000 contribution limit is for IRAs and Roth IRAs combined in 2024, so you can’t contribute $7,000 to each.

While the SECURE Act 2.0 changed the composition of the IRA catch-up contribution to include annual cost-of-living adjustments, the IRA catch-up provision for 2024 will remain at $1,000. That means you can make a maximum contribution of $8,000 to your IRAs if you include the full catch-up.

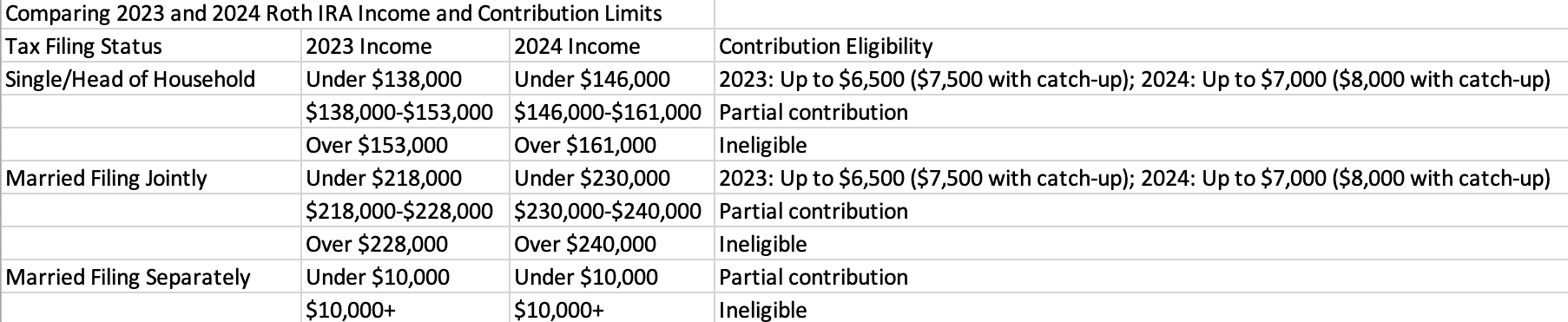

2024 Roth IRA Income Limits

There are income limits that you need to fall within to make full or partial contributions to Roth IRAs. Those income thresholds are based on your Modified Gross Adjusted Income and are increasing in 2024.

For 2024, your MAGI needs to be lower than $230,000 if you’re married and filing jointly. You can still make a partial contribution if your MAGI is under $240,000. That $230,000-$240,000 phase-out range is up from $218,000-$228,000 in 2023. If you’re a single filer contributing to a Roth IRA, your MAGI needs to be below $146,000 to make a full contribution (and $161,000 for a partial contribution). That $146,000-$161,000 range is up from $138,000-$153,000 in 2023. Check out the full breakdown in Figure 2.

FIGURE 2 – Comparing 2023 and 2024 Roth IRA Income and Contribution Limits – IRS

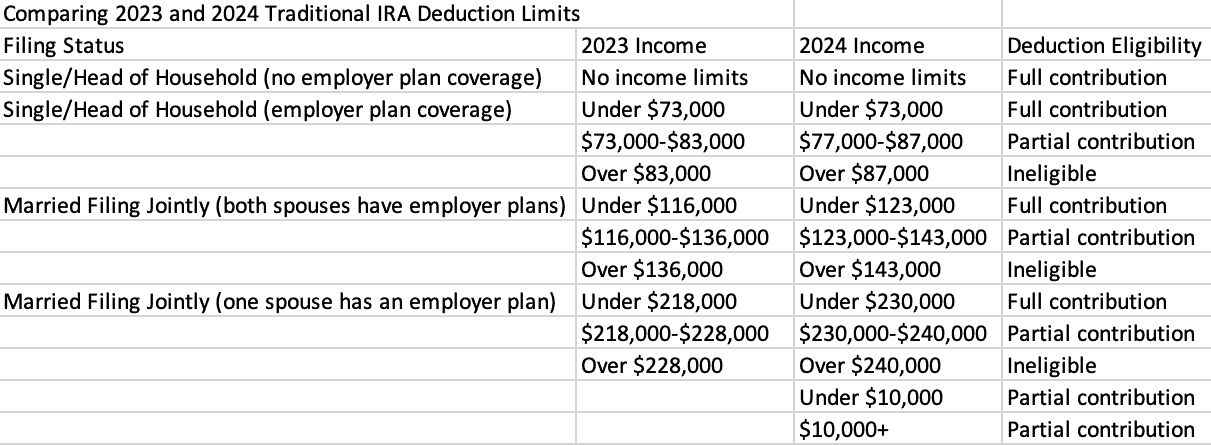

2024 Traditional IRA Deduction Limits

Now, let’s shift gears to 2024 traditional IRA deduction limits. These will vary depending on if you and your spouse have workplace employer plans. If you want to make a contribution and your spouse has coverage, you’ll be eligible to make a full contribution if your income is less than $123,000. That limit is currently $116,000 in 2023. You will still be eligible for a partial contribution if it’s less than $143,000.

If you want to make a contribution and don’t have coverage, but your spouse has a workplace plan, you can make a full contribution if your income is under $230,000. That threshold is $218,000 in 2023. You’ll still be eligible for a partial contribution if it’s under $240,000.

For those who have a workplace plan and are single filer, your phaseout range will be between $77,000-$87,000. That’s up from $73,000-$83,000 in 2023. There are no income limits if you’re a single filer and don’t have a workplace plan. See Figure 3 below for a rundown on 2024 traditional IRA deduction limits.

FIGURE 3 – Comparing 2023 and 2024 Traditional IRA Income and Deduction Limits – IRS

2024 IRA Contribution Limits for Small Business Owners and Self-Employed Individuals

Don’t worry, we didn’t forget about the 2024 IRA contribution limits for small business owners and self-employed individuals. If you contribute to a SIMPLE IRA, you can contribute up to $16,000 in 2024. That’s up from $15,500 in 2023. There’s also a $3,500 catch-up provision, so your maximum contribution can be $19,500 if you’re 50 or older.

There are two contribution limits to keep in mind for those with SEP IRAs. You can contribute $69,000 in 2024, which is up from $66,000 in 2023. SEP IRA contributions also can’t be more than $25% of your compensation. In regards to how much you’re eligible to contribute to your employee’s SEP IRAs, you need to follow the 25% compensation limit, which is limited to $345,000 for 2024. That’s up from $330,000 in 2023. It’s worth noting the SEP IRAs don’t have catch-up contributions.

Other Changes to 2024 Retirement Plan Contribution Limits Due to SECURE 2.0

There are a few other important provisions from the SECURE Act 2.0 that are related to the 2024 retirement plan contribution limits. One change relates to charitable distributions. If you’re charitably inclined, you might be pleased to learn that the annual deduction limit on charitable distributions will increase from $100,000 to $105,000 in 2024.

Another change involves the deductible limit for one-time elections to treat IRA distributions directly from a trustee to a split-interest entity. That threshold will increase from $50,000-$53,000 in 2024.

Do You Have Any Questions?

Maximizing your annual 401(k) and IRA contributions is important as you’re saving for retirement. As you’re planning for retirement, don’t hesitate to reach out to us with any questions regarding how much you need to save for retirement, where you’re saving for retirement, the 2024 401(k) and IRA contribution limits, etc. You can start a conversation with us by clicking the button below.

To get clear answers to those questions, you’re going to need a comprehensive financial plan that takes you to and through retirement. It’s our job to build you a goals-based plan that can give you more confidence that you’re doing the right things with your money, freedom from financial stress, and time to spend doing the things you love. We’re excited for the opportunity to work with you to build that plan for you and to show you how maximizing your 401(k) and IRA contribution limits can be a key part of it.

Resources Mentioned in This Article

- Optimizing Your 401(k) for Retirement with Drew Jones

- Financial Planning for Veterans

- 10 Ways to Fight Inflation in Retirement

- Revisiting Roth vs. Traditional with Bud Kasper and Corey Hulstein, CPA

- Understanding the SECURE Act 2.0 with Ed Slott

- Social Security Administration Announces 3.2% COLA Increase for 2024

- Retirement Planning for Self-Employed Individuals and Small Business Owners

- Charitable Giving in Retirement

- Retirement Savings by Age

- How Much Do I Need to Retire?

- Where Should I Be Saving for Retirement?

- Starting the Retirement Planning Process

- Components of a Complete Financial Plan with Logan DeGraeve

- Financial Stress: How Do You Deal with It?

Schedule a Complimentary Consultation

Click below to get started. We can meet in-person, by virtual meeting, or by phone. Then it’s just two simple steps to schedule a time for your Complimentary Consultation.

Investment advisory services offered through Modern Wealth Management, LLC, an SEC Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management an SEC Registered Investment Adviser. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.