6 Reasons Roth Conversions Could Work for You

Key Points – 6 Reasons Roth Conversions Could Work for You

- Roth Conversions Are One of the Most Popular Tax Planning Strategies

- How Can You Get Roth Conversions at a Discount?

- The Five-Year Rule(s) with Roth Conversions

- Doing Roth Conversions While You’re in the Lowest Possible Tax Bracket

- 8 Minutes to Read

A Recession Could Be Coming … Could This Be a Good Time for a Roth Conversion?

If you read our blog post from earlier this month titled, 8 Ways to Prepare for a Recession, you might remember that Roth conversions were No. 1 on the list. While Roth conversions aren’t for everyone, there are quite a few reasons why they could be right for you.

We’re going to review these six reasons to help you make the most educated decision about Roth conversions.

- Taking Advantage of Discounted Roth Conversions

- Starting Your Five-Year Clock

- Income from Your Roth IRA Doesn’t Cause Your Social Security to Become Taxable or Increase Your Medicare Premiums

- No Required Minimum Distributions After Doing Roth Conversions

- Roth Conversions Can Be a Part of Your Tax Bucket Strategy

- Leaving a Legacy with the Help of Roth Conversions

We want to you have clarity and confidence about your financial life despite these uncertain times in the markets, so it’s important to know whether doing a Roth conversion can help you with that.

1. Taking Advantage of Discounted Roth Conversions

If you’re feeling stressed about the bear market we’re going through, you’re not alone. People who are closing in on retirement and recent retirees are among those who have been the most concerned about this bear market, especially if they don’t have a financial plan. We’re hopeful that retirees and pre-retirees not only understand how critical it is to have a financial plan right now, and that they realize that a financial plan isn’t complete without proper tax planning. One of the most popular tax planning techniques just happens to be Roth conversions.

Looking at Current and Future Tax Rates

While market downturns are far from ideal, they do create opportunities for Roth conversions and other tax planning opportunities. However, it’s not a guarantee that a Roth conversion will be the best decision for your tax situation. It all depends on what your tax rate is today and what you anticipate it to be in the future.

In most cases, it makes the most sense to make contributions to a traditional IRA if your current tax rate will be higher than your future tax rate when your funds are withdrawn. On the flip side, Roth contributions or conversions make a lot more sense when the current tax rate is projected to be lower than what it will be in the future.

How Can Roth Conversions Be Discounted?

If you are thinking about making a Roth conversion right now, obviously this declining market factors into the decision. Given how lackluster market performances have been in 2022, the “Taking Advantage of Discounted Roth Conversions” headline probably grabbed your attention. So, how can Roth conversions come at a discount?

Declining markets can essentially put a Roth conversion at a temporary discount because when the overall account’s value declines, the amount getting converted to a Roth account will account for a bigger portion of the pre-tax account. This results in a bigger percentage of the account’s future growth transitioning into a Roth despite not going into a higher tax bracket as a larger portion of the account is converted.

Using Apple Stock as An Example

We’re going to look at Apple as an educational example because we believe this is valuable for our reader in light of the current economic and market conditions so far in 2022. We do not consider this example to be investment advice. As always, consult your financial professional before making any financial decisions.

Dating back to March 29, Apple’s value was all the way up at $178.96 per share. By June 16, its value had dropped all the way down to $130.06 per share.

If you converted $50,000 of Apple stock on March 29, you could’ve had converted 279 shares. If you converted the same amount on June 16, you could have converted 384 shares. Apple stock has been back on the rise over the past month, now sitting comfortably over $150 a share. But by doing a Roth conversion when markets are still down, it speeds up the upswing when they do start recovering. And remember, it’s tax-free, too!

2. Starting Your Five-Year Clock

In our next reason that a Roth conversion could be right for you, we look at starting that five-year clock. As it pertains to the five-year rule, “earnings” on Roth contributions and Roth conversions are treated in pretty much the same fashion. For each Roth conversion, you need to be 59 ½ years AND wait five years from January 1 in the year the conversion took place to withdraw tax/penalty free. So, if you want that tax-free income in retirement, you need that five-year clock rolling. It could also be beneficial to do larger Roth conversions earlier on because of the five-year rule.

For example, if you made a Roth conversion in 2017, the clock on the five-year rule starts from January 1, 2017. Switching custodians is not considered a conversion or contribution and therefore the five-year rule is unaffected by this.

Misconceptions About the Five-Year Rule

There are a few misconceptions about the five-year rule, though. Let’s review them.

- There is a belief that the five-year rule applies to each Roth IRA separately. That’s not true.

- People also get concerned rolling over to another Roth IRA reset the five-year clock. That’s also not true.

There’s also another five-year rule with Roth IRAs, so make sure that you don’t get them confused. The other five-year rule involves the 10% early distribution penalty. For this five-year rule, the 10% penalty isn’t enforced if a minimum of five tax years have passed after the distribution of principal from the converted IRA.

3. Income from Your Roth IRA Doesn’t Cause Your Social Security to Become Taxable or Increase Your Medicare Premiums

As we continue to look at how Roth conversion could be right for you, we’d be remiss if we didn’t go to America’s IRA expert, Ed Slott, for his insight. Along with coming to Kansas City for Ed Slott’s Elite IRA Advisory Group℠ Workshop, Ed appeared in person on the Guided Retirement Show.

On that episode, Ed shared two different points that we’ll consolidate to one here. Both of them can oftentimes be benefits of Roth conversions that advisors don’t immediately think about. The first one is that income from your Roth IRA doesn’t impact how much your Social Security is taxed. As Financial Advisor magazine also points out, Roth conversions can lower assets in tax-deferred accounts, which can help with avoiding higher Social Security taxes later in retirement.

Looking at the Big Picture of Retirement

If you couldn’t tell from the benefits of the five-year rule, looking at what Roth conversions can do over the course of your retirement rather than in the short term is critical. That ties in with Ed’s other reason that Roth conversions could be right for you. That other reason is that Roth IRA income doesn’t increase your Medicare premiums.

Ed remembers how someone at a seminar expressed to him that she was worried about doing a Roth conversion because her IRMAA—her Parts B and D premium surcharges—were going to go up significantly that year. Ed encouraged her to do the Roth conversion anyway because of the benefit she would get later.

4. No Required Minimum Distributions After Doing Roth Conversions

That woman’s concern led right into another point that Ed had about why a Roth conversion could be right for her (and others). If she had elected not to do a Roth conversion, she was going to be forced to take Required Minimum Distributions starting at age 73. But with Roth IRAs, RMDs don’t apply. Now, hopefully you can begin to see the big picture that Ed was alluding to.

5. Roth Conversions Can Be a Part of Your Tax Bucket Strategy

Speaking of having a long-term perspective, there’s something that’s coming up in 2026 that will change the tax planning game in a big way. We’ll be going back to the tax rates from 2017 since the Tax Cuts and Jobs Act will be sunsetting. That means rates will be rising after 2025. Doing a Roth conversion now and mitigating as much as you can in taxes before 2026 while tax rates are lower by doing a Roth conversion could be in your best interest.

To get an idea of what to be preparing for in 2026, let’s look 2017 and 2021 tax rates.

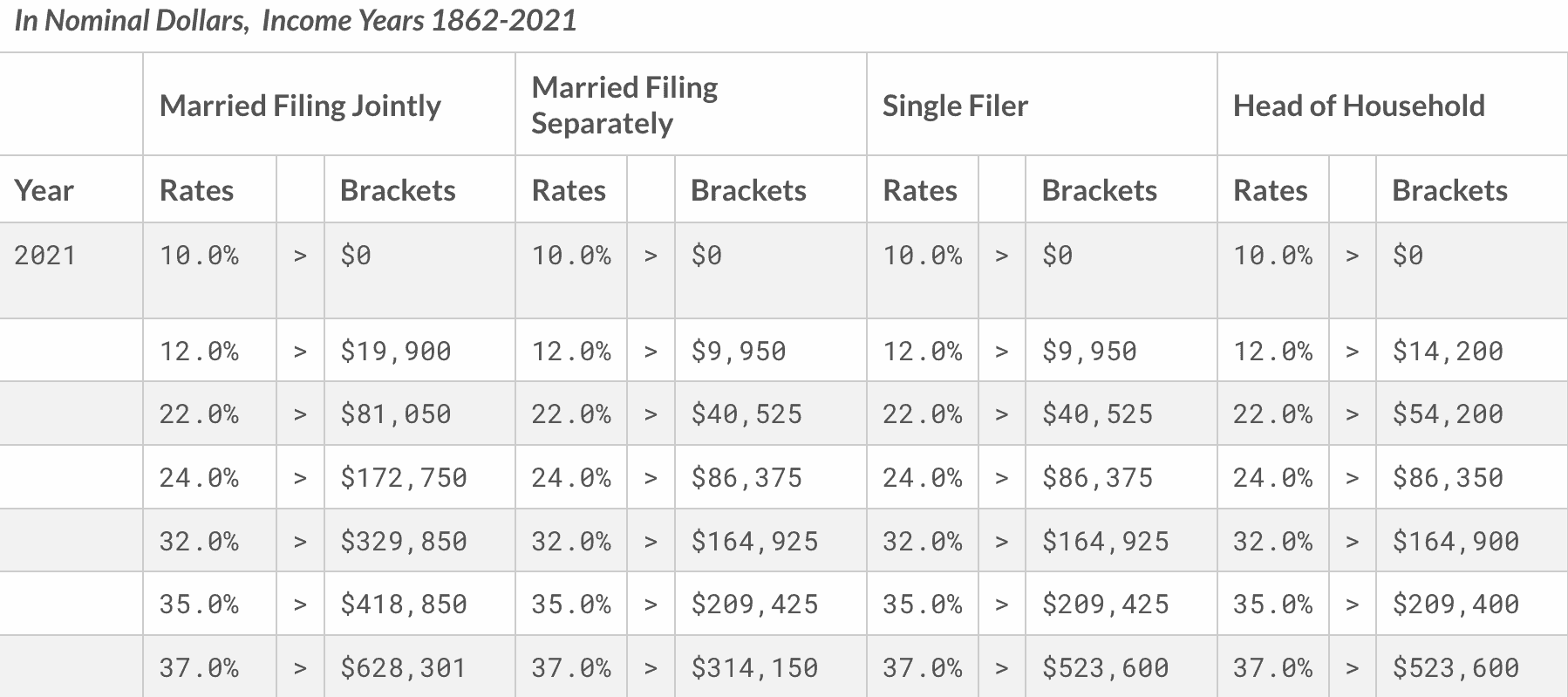

FIGURE 1 – 2021 Tax Rates – Tax Foundation

FIGURE 2 – 2017 Tax Rates – Tax Foundation

A Tax Bracket Blast from the Past

We’ll discuss this more momentarily, but hopefully this helps highlight how big of a deal tax bracket management is. Before we share about the role Roth conversions play in that, let’s look back at a few more years just to gain a better perspective of how tax brackets have changed over the years.

FIGURE 3 – 1992 Tax Rates – Tax Foundation

As you can see in Figure 3, there were only three tax brackets in 1992. This was right before the Omnibus Budget Reconciliation Act of 1993, which saw a shift to five tax brackets (15%, 28%, 31%, 36%, and 39.6%).

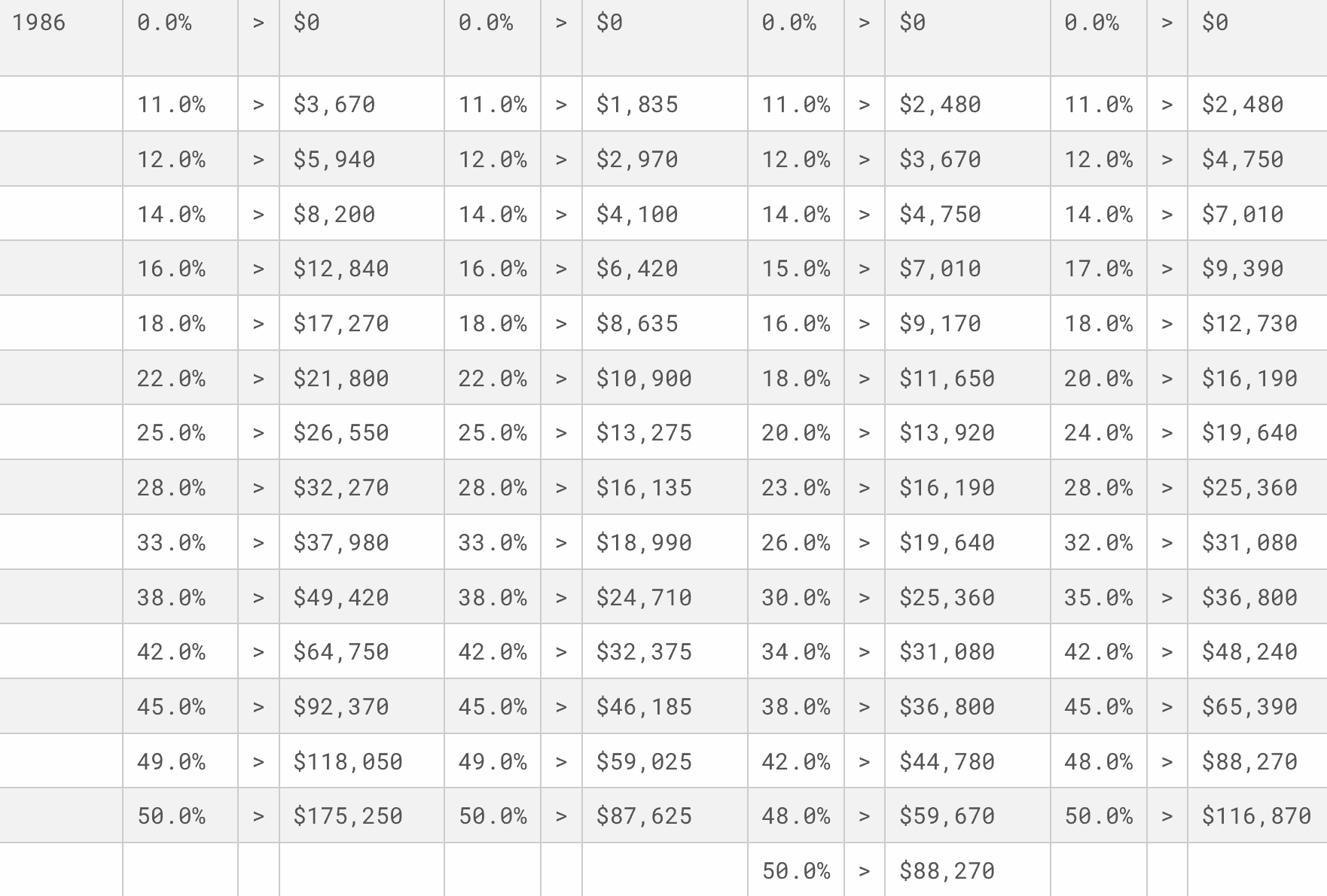

FIGURE 4 – 1986 Tax Rates – Tax Foundation

My what a difference six years makes…. The Tax Reform Act of 1986 took the top tax rate for ordinary income from 50% down to 28%, while the bottom tax rate went up from 11% to 15%. This marked the first time that the top tax rate went down and the bottom rate went up simultaneously.

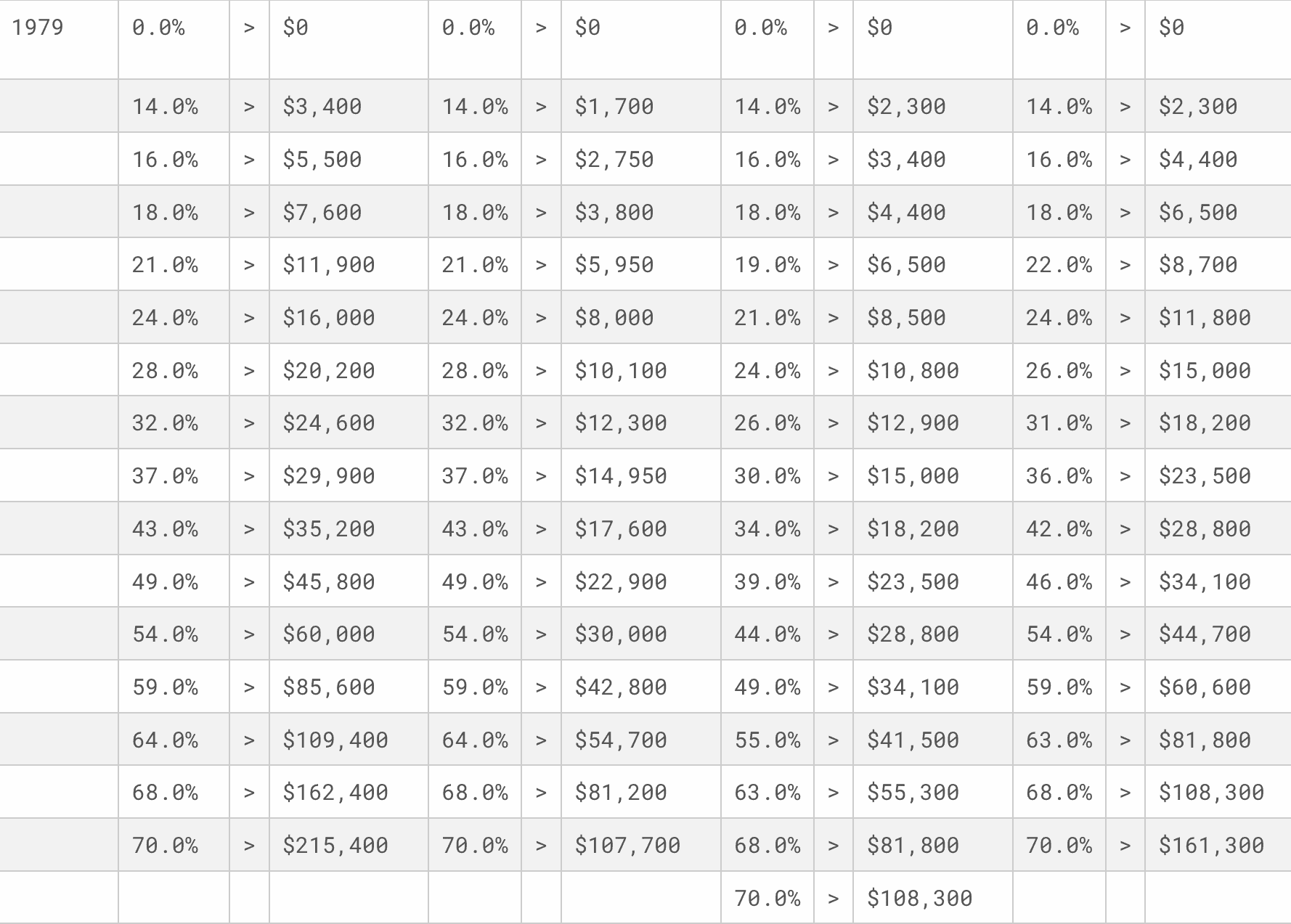

FIGURE 5 – 1979 Tax Rates – Tax Foundation

Just to give you an idea of how many different tax brackets there were for most of the 20th century, I couldn’t capture all the tax brackets in one laptop screenshot from 1917-1978. If you want to have some fun looking at a history of tax brackets, Tax Foundation has records of them dating all the way back to 1862. Which tax bracket do you think you would’ve been in in 1862?

FIGURE 6 – 1862 Tax Rates – Tax Foundation

Breaking Down Tax Bracket Management

Tax bracket management is something that always needs to be top of mind while you’re reviewing your financial plan. If you happen to be in a lower tax bracket, you can still reap the rewards of Roth conversions. Here’s an example of why that’s the case. Let’s say that you’re married filing jointly and your taxable income is less than $178,000, you’ll be in the 22% bracket. You will also stay in the 22% bracket if you have $128,000 in taxable income and convert $50,000 of a Roth IRA.

So, why does that matter? To understand why that matters, you need to project what your total income will be in retirement. We’re not just projecting your income for the early years of retirement, but long term after you turn 73. Again, it’s all about the big picture. You need to see what tax bracket you’ll be in year after year.

When a lot of people need to start taking RMDs, that might bump them to the 24% or 32% bracket. So, it might be the right choice to do that Roth conversion now while you’re still in the 22% bracket to take advantage of that tax-free growth. The money in your IRA needs to come out at some point, and the goal to take it out at the lowest tax rate possible. Roth conversions can be a way that you do that.

One of the key takeaways here is that Roth conversions aren’t an all or nothing thing. Doing methodical Roth conversions to stay in the lowest possible tax bracket is a big reason why you need to take a year-by-year approach.

6. Leaving Your Legacy with the Help of Roth Conversions

Last, but not least, we know how important it is to many pre-retirees and retirees alike to leave a legacy. The tax-free aspect of Roth conversions not only can be beneficial for you, but the rest of your family as well. God forbid if you pass away and your spouse or child becomes the account owner of your Roth IRA, the same rules apply to them. It will be totally tax-free for them if it was held for the five-year period we mentioned earlier.

Reach Out to Us with Your Roth Conversions Questions

These are just a few reasons why Roth conversions could be right for you. However, we want you to be 100% sure of your decision. To help give you that clarity that’s essential to living your one best financial life, you can use our industry-leading financial planning tool—the same tool that we use with our clients—from the comfort of your own home at no charge. Just click the “Start Planning” button below to begin building your plan. Maybe a Roth conversion could be a key part of it.

There are a lot of moving parts to a comprehensive financial plan. While Roth conversions could make your financial life easier, there are no do-overs in retirement. If you have any questions about Roth conversions, our financial planning tool, or anything else regarding your retirement, you can schedule a 20-minute “ask anything” session or a complimentary consultation with CERTIFIED FINANCIAL PLANNER™ Professionals. We can meet with you in person, by phone, or virtually—whatever works best for you.

Investment advisory services offered through Modern Wealth Management, Inc., an SEC Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management an SEC Registered Investment Advisor. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.