Bear Market Is Here, Is There More to Come?

Key Points – Bear Market Is Here, Is There More to Come?

- Back to Bear Market Rallies

- An Example of a Building a Comprehensive Plan

- Market Valuations and Interest Rates

- Finding Clarity in Chaotic Conditions

- 21 minutes to read | 38 minutes to listen

The S&P 500 entered bear market territory, preceded by the NASDAQ index entering bear market territory a few weeks back. Join Dean Barber and Bud Kasper as they discuss navigating the current bear market.

START BUILDING YOUR PLAN CONNECT

Show Resources:

Find links to the resources Dean and Bud mentioned on this episode below.

- Download: Retirement Plan Checklist

- Schedule: 20-Minute “Ask Anything” Session

- Education Center: Articles, Videos, Podcasts, and More

Bear Market Is Here, Is There More to Come?

Dean Barber: All right, Bud, it’s officially a bear market. Look, the NASDAQ’s been in a bear market for a while.

Bud Kasper: True.

Back to Bear Market Rallies

Dean Barber: S&P 500 entered into a bear market. I think it was two weeks ago that we did the show about bear market rallies, and as we were doing that show, the market rallied by about 4% or 5% within just two or three days.

After that, in five days, the market fell almost 10%.

Bud Kasper: A dead cat bounce.

What if..?

Dean Barber: Look, you and I have been through this many times, Bud, and history is a good teacher. So, what I want to talk about today is understanding what you own in your portfolio and whether or not what you own in your portfolio can take you through an actual full-blown bear market.

Because at this point, 21% down on the S&P 500 feels nasty, but what happens if it’s 40%? What happens if it’s 45% or 50%? What happens if it’s 70% on the NASDAQ like it was back in the Dot-Com Bubble? How will that impact your portfolio? Or, more importantly, what does that do to your ability to get to and through retirement? And I think that’s the real question we have to ask Bud.

Bud Kasper: It is without a doubt. And fortunately, we do have the tools to basically take your temperature, if I may use this expression.

But we should be doing it before the event occurs.

Dean Barber: No kidding!

An Example of a Building a Comprehensive Plan

Well, so here’s what you do, Bud. Let’s paint an example here. We’re going to assume that those of you reading have done a financial plan, a comprehensive financial plan like our Guided Retirement System™. That means you’ve entered in your plan exactly how much you want to spend and when you want to spend it.

What’s in a Comprehensive Plan?

Your plan also accounts for what inflation could be. You’ve factored in all your budgeting items throughout your retirement, vehicle replacements, trips, gifts to kids and grandkids, college education for grandkids if you want to help fund your legacy goals, etc.

There’s a whole bunch that goes in. There’s a whole bunch that goes into the budgeting piece. You’ve adequately entered in how much you have in taxable, tax-deferred, and tax-free accounts. You’ve adequately entered what Social Security will be and how and when to claim.

In your plan, you have calculated what your tax liabilities will be every year. You factored in literally everything that you want to happen in your financial life.

Probability of Success

Then, once you’ve done all that, at the very end, you say, “Okay, here’s the money that I have, and here’s the actual asset allocation of what I have today.” And your plan then says, “Oh, you’re at an 85% probability of success.” Well, what does that mean?

It means that from a historical perspective, using a Monte Carlo simulation, you could spend 85% of the time as you outlined in your plan without alteration, keeping up with inflation, etc. Fifteen percent of the time, you may have to adjust your spending for a period because it won’t be able to be what you outlined in that plan.

If you’re at an 85% probability of success, we call that being in the comfort zone. So Bud, from a mathematical perspective, if someone’s sitting in front of us and we’ve gone through the planning process, and they’re showing an 85% probability of success, we’re going to say, “You know what, you’re fine. You’re in good shape. You don’t need to change a thing.”

But then comes the human emotion and the psyche of what’s happening in the markets. And if it’s too uncomfortable, then what we do is we try to identify the Goldilocks portfolio. The Goldilocks portfolio is the one that’s just right for you, where we can reduce the risk substantially and still have your probability of success remain the same.

Adjusting the Numbers, Goldilocks Portfolio

When you use the program we use, you can dial up the risk by saying, “Hey, what happens if I have a 100% in stocks? What’s that do to my probability of success?” In our example at 85%, your probability of success may have gone down to 70% if you’re 100% in stocks. So, that’s too much. So you start reducing the stock exposure and entering in cash and bonds and say, “What’s the magic mix, and how little can I have in stocks and still keep that probability of success at 85%?” That’s your Goldilocks portfolio.

Now there can be periods when people can take their money and get safer—just understand that eventually, you’ll have to have a growth engine back in that portfolio.

Bud Kasper: The difficult part is not letting your emotions get in the way. And one of the ways we can help eliminate that is to make sure that we stress test your financial plan so that you can agree that you’re in the right place.

We always ask, “All right now, if your portfolio were to lose 20%, what would your reaction be? Would you sell everything in the various options available to you?” And people almost always came back, “No, no, I’ll just hang in there and let it ride through.”

Dean Barber: But it’s a different story when it’s happening.

Bud Kasper: It sure is.

Market Valuations and Interest Rates

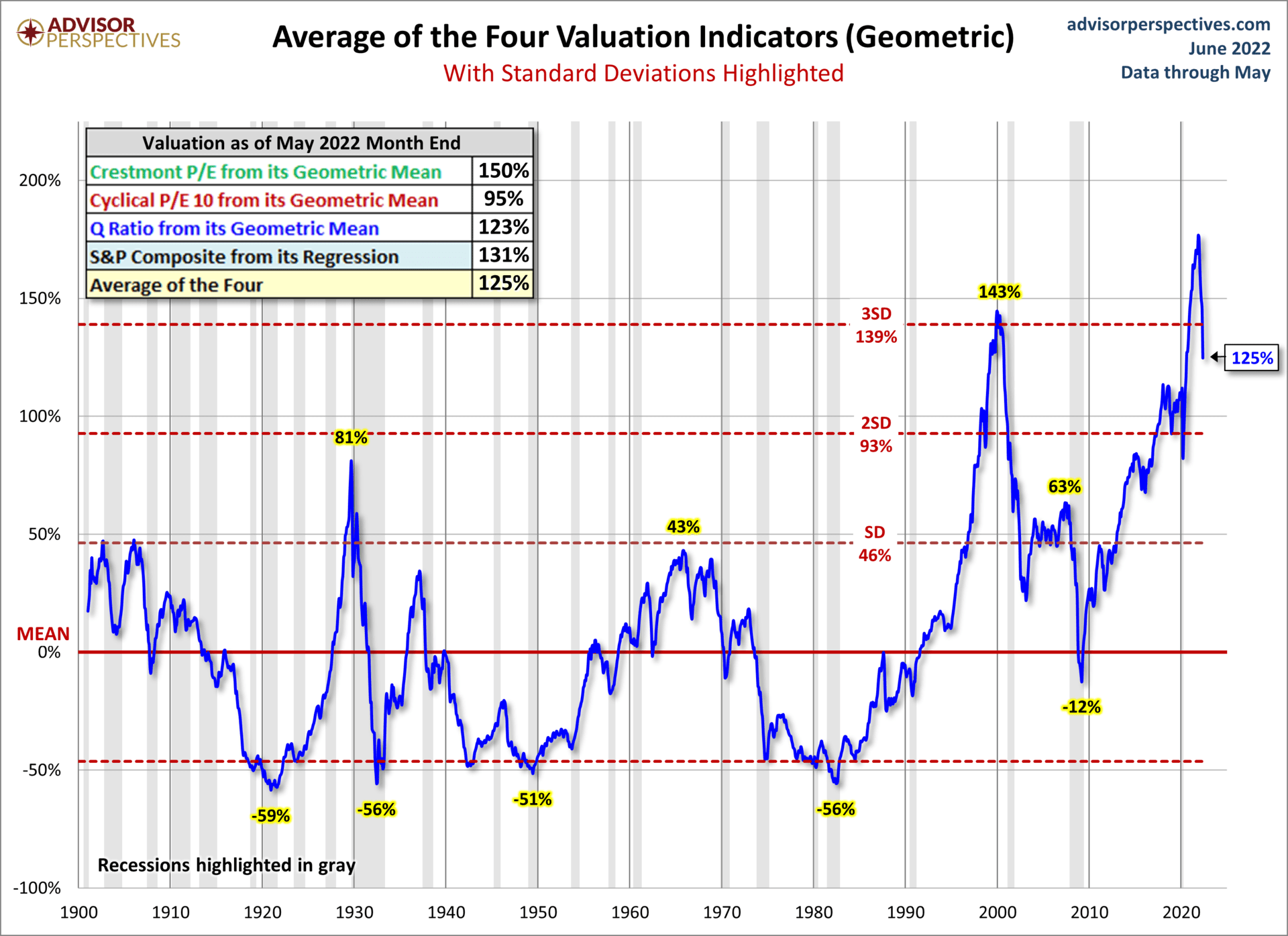

FIGURE 1 | Is the Market Still Overvalued? | Advisor Perspectives

Dean Barber: Bud, just look at this chart, Bud. Look at this chart in Figure 1. We’ve been talking about this now, literally for over six months. We were talking about how the equity markets were severely overvalued. And think about this, Bud. When you look at this chart, what was the argument for the valuation of stocks being that high? Well, interest rates are so low that they can support those valuations.

Interest Rates in 2022

What’s happening with interest rates? The Fed is planning to get the Fed funds rate somewhere between 3% and 3.5% by the end of the year.

But if you take these four valuation indicators in Figure 1, Crestmont’s P/E, you look at the cyclical, P/E 10, the Q ratio, and the S&P Composite from its regression. Figure 1 goes back to 1900, and before the Great Depression started in 1929, when you use an average of these four valuations, the equity markets were 81% overvalued. When we hit the Dot-Com Bubble, the equity valuations were 143% above fair value.

January of 2022, they were over 170% above fair value. At the end of May, they were 125% above fair value. They’re not 125% above fair value anymore, Bud, because we’ve had more drawdown here in June. The point is that if we just get back to 63% above fair value, which is where we were right before the Great Recession, there is pain ahead of us.

Stress-Testing Through Historical Bear Markets and Recessions

So with the valuations where they are today, at valuations not seen since the Dot-Com Bubble, the only way that you’re going to be able to know, “Am I okay? Can I do the things I want to do?” You’ve got to go back and pretend that you’re going to retire on January 1, 2000, and you’re going to go through the Doc-Com Bubble and the Great Recession because it took both of those to get the valuations back to the mean.

And Bud, we referred to that as the lost decade.

Bud Kasper: It was. And the thing is, as we do the stress test, we go through those periods so our clients can visually see the negative impact that the market has from time to time. Now-

Dean Barber: We want to ensure your plan can weather it, right?

Overstimulus from COVID

Bud Kasper: When I think about it, though, it’s more in the flaw of the leadership inside the Federal Reserve. What I mean by that is if they didn’t overstimulate, which we know they did with COVID. And thank God they didn’t get through the $6 trillion package they were asking for because I can’t imagine the disaster we’d have experienced.

Dean Barber: No, no, no, no. You’re mistaken here, Bud. It has nothing to do with stimulus. The printing of money doesn’t cause inflation. It’s Putin!

[Laughter]

Bud Kasper: He’s sarcastic, ladies and gentlemen, with this.

Reducing Risk

I’m venturing out here, though, because it was so apparent that it was overvalued. Most certainly, we should have been taking additional measures to be able to reduce risk.

We do that periodically predicated upon the overarching plan in what we’re trying to accomplish in realizing that when we go through these periods, we have to have that safe money to continue to do distributions for those taking distributions.

Then, we need to be able to have the other in a position to be able to continue to grow. Granted, these are uncomfortable times we’re living through right now, but by making little adjustments inside the plan, we weather these storms rather well.

The Sun Will Come Out Tomorrow

Dean Barber: Well, and here’s the point, the sun will come out again tomorrow. We can go back and say, “Hey, eventually we’ll get on the other side of this,” but there will be a washout before we get there. And there will be people who just ignore it and say, “I’m not going to think about it. I’m not going to open my statements.”

Okay, big mistake, big mistake. You can’t do that in times like this. You must pay attention to what you own, why you own it, and how it will react during different market cycles.

Forward-Looking Financial Planning Takes Time and Effort

Look, if you’ve done the financial plan, not back-of-the-envelope math or taking the value of your portfolio and multiplying it by 4% and saying, “That’s my distribution rate.” and putting that in the Excel spreadsheet. That’s not a financial plan.

You have to consider every aspect of your financial life as you look forward and that financial plan is designed to be a forward-looking plan.

And if you’ve done that and your asset allocation today shows your probability of success is in the comfort zone or even higher, then you have nothing to worry about. Then you have to ask yourself, “Could I still have that success by taking some risk off the table so that I can sleep better at night and maybe be a little more comfortable?”

Bonds Aren’t Our Friend Right Now

Bud Kasper: You know, Dean, when we look at history, there’s been 14 bear markets since World War II. And on average, the S&P 500 is pulled back approximately 30% in each of those. And they lasted on average 359 days, so about a year. If we look at where we started this year, are we about one-third through this if we’re going back to the mean? I think so, probably. What’s difficult this time around is that bonds are not our friend.

Dean Barber: And they can’t be.

Bud Kasper: They won’t be for a while, but as these interest rates start to rise, which contradicts some of the possible returns on the market. Of course, it’s taking value away from bonds, but it’s raising the potential for more income in the future.

The timing of that, and I use that cautiously, suggests that we could be locking in some pretty decent returns. If we look at an investment that you and I are familiar with, the symbol is STIP. It’s zero to five-year maturity of Treasury Inflation Protection Securities.

It goes up every time the Federal Reserve makes a move. If you look at it today, it’s over 6%. Now, 6% is a nice return.

What About Annuities?

So many salespeople are selling annuity fixed income and all that stuff. Let me tell you when you lock in, and you get, let’s say, a 3% fixed guaranteed income base, and you factor in inflation on top-

Dean Barber: You’re going backward.

Bud Kasper: You are flat to backward. That’s right. All you did was allow fear to come into your life, to take the worry away from what the market is doing, opportunity, ladies and gentlemen. I have been doing this for 38 years is going to be borne out of this situation. It’s uncomfortable, but if you’re working with the right people, I’ll say this one more time. If you’re working with a person who knows how to do financial planning, and usually that’s going to be a CERTIFIED FINANCIAL PLANNER™ professional, then you should be in pretty good shape.

Dean Barber: Yeah, you’re right, Bud. And look, the last thing you want to do in a time like this is panic and lock your money up into something that will sometimes tie it up for 7, 8, 10, or 12 years. That’s not a smart decision, and it may make you feel better initially. But when the opportunity to start to make money again comes back and you’re stuck, you will be upset. So don’t make emotional decisions.

Start Building Your Plan Today

Look, you can do this. Bud and I do this, and we’ve been doing this 35 years for me, 38 years for Bud. And we got a lot of experience behind all of the CERTIFIED FINANCIAL PLANNER™ professionals here at Modern Wealth Management.

So, we know how to do this. We’ve been through it before. Bud, I have clients I reviewed this last week that retired just before the Great Recession, and you know what? They’re still retired, spent everything they intended to spend, and are in good shape.

So you don’t have to panic. You just have to know what to do. It’s like the checklist that the pilot that’s flying the plane if something happens, what’s my next step? And that’s part of building out the financial plan and working with a CERTIFIED FINANCIAL PLANNER™. You can start building your plan from the comfort of your home here.

The Fed’s Radical Changes

Dean Barber: Oh boy. The Fed is taking a walk on the wild side.

Bud Kasper: It sure is. Some radical changes.

Dean Barber: Well, think about some of the headlines we see today, Bud. Mortgage demand is half of what it was a year ago. You and I did a show about a month and a half ago where we were talking about the 30-year mortgage rate. The anticipation is that the 30-year mortgage rate could be as high as 6.75% by the end of this year. We haven’t seen those numbers since before the dot-com bubble, Bud.

Bud Kasper: Yeah. It sure is. Here’s another situation that becomes negative to the economy. Economic growth will slow because housing will slow because of higher interest rates.

Dean Barber: Let’s get to some of the causes of what’s happening in the stock market today. We can also talk about the reasons for what’s going on in the bond market. The Fed has a very, very difficult situation to navigate through. You and I have been talking about that all year long.

We talked about how we felt that the Fed should have started raising rates last year, but they didn’t because they said that inflation would be transitory. That was the assumption that inflation was caused simply by supply chain issues.

Bud Kasper: That was huge.

Inflation, Recession, and Stagflation

Dean Barber: That was a big deal, and that was the assumption. The reality has turned out to be something entirely different. We see today inflation running at a pace that it hasn’t done in 40 years. At the same time, we see an economy that is stagnating, Bud.

We had a negative GDP number in the first quarter, negative by 1.5%, which means that the economy contracted by 1.5% in our gross domestic product in the first quarter of 2022. The estimate for the second quarter of 2022 is an expansion of nine-tenths of 1%, so 0.9%.

If that proves to be negative, that officially puts the economy into a recession because the definition of a recession is two consecutive quarters of negative GDP growth.

Bud Kasper: We’re there.

Dean Barber: We could very well be there. We won’t know until late July when the first estimates for the GDP come out, and then there will be a second and final revision for GDP numbers. The bottom line is that we’ve got a stagnating economy, and we’ve got high inflation, and we’ve got rising interest rates. What is that doing to corporate profits?

This year we will likely see the highest increase in wages across the board in the last 40 years in a single year. Because if you just go to your cost of living increase, those cost of living increases are going to be 5% to 8% across the board. What’s that going to do to corporate profits, Bud?

Bud Kasper: It’s going to take it down.

Dean Barber: That’s going to take it down. We’ve now got higher borrowing costs for corporations. What’s that going to do to corporate profits? It’s going to reduce it, right?

Bud Kasper: Right.

Two Choices for the Fed’s Monetary Policy

Dean Barber: You have supply chain issues. You’ve got shipping costs. You’ve got raw material costs. Across the board, there are all kinds of things that are squeezing on corporate profits.

Of course, when you’re looking at market valuations, like what we were talking about last time if market valuations are where they are today based on forward-looking estimates from these companies because it’s a forward-looking price to earnings ratio. It’s not what it is today.

If these companies miss their estimates because of the increased labor cost, supply chain issues, higher borrowing costs, et cetera, what do you think that’s going to do? It will bring the market down more because the prices have to come back down to a more normal valuation, and they’re nowhere close to that.

Bud Kasper: The takeaway is that the stock market is being held hostage by what the Federal Reserve is doing.

Dean Barber: The Fed has two choices. The Fed has two options. We could say, “You know what, we don’t want a recession. We don’t want a squeeze on corporate profits. We’re going to go back to our easy monetary policy. We’re going to reduce rates here soon, and we’re going to-”

Bud Kasper: Which got us into this, to begin with.

Dean Barber: “We’re going to give more stimulus. Forget about inflation.” Well, who does that hurt? It hurts the average American. Inflation is hurting the average American in significant ways, Bud. The Fed can’t do that.

The Fed the put that in place since the Great Recession is gone.

Bud Kasper: Gone.

Dean Barber: It’s gone.

Bud Kasper: Taken away.

Dean Barber: The Fed isn’t going to protect the markets this time. They can’t.

Bud Kasper: No. That’s because inflation is a bigger issue.

Finding Clarity in Chaotic Conditions

As you mentioned a moment ago, look at the chip shortage and the supply chain. When you look at China, that’s shut down because they don’t use vaccines over the COVID situation. They just shut down cities requiring people to stay inside their apartments. This means that they’re not manufacturing. Which means that it gets into the supply chain. High-interest rates.

Bud Kasper: You’re exactly right. These issues, it’s not that we haven’t seen this before. It’s just that it feels so darn crummy when we’re going through it. You got to look past it.

Dean Barber: How you do that, once again, and I can’t emphasize this enough, you have to have your financial plan built, and you have to stress-test it through these uncertain economic times. Because this isn’t the first time, we’ve had an uncertain economy. It’s not the first time we’ve had a shaky stock market. It’s certainly not going to be the last.

As long as you are alive and have money and need to grow that money to support you in retirement, you need to understand the ins and outs of the financial plan and how you get through those difficult times, and how you can do it with a high degree of confidence and clarity.

We want to allow as many people as possible to get that clarity. We’ve opened up the ability for you, the individual listener out there, to build your plan using the same state-of-the-art software we use to develop the plan.

Begin to build your plan from the comfort of your own home. There’s no cost here. There’s no obligation, nothing like that. We want you to get clarity. We want you to gain control over what’s happening in the economy and your life.

Patience is Key During a Bear Markets

Bud Kasper: I think this ultimately will be a game of patience because these cycles have occurred, as they said, 14 bear markets. The similarities in terms of the depths of these changes, sometimes more radically than others, but the net result is, as I said before, 359 days is the average before returning to recovery.

Dean Barber: I don’t like that average number.

Bud Kasper: No?

Dean Barber: I don’t. I don’t. Look at where valuations are today. Then we’re in a rising interest rate environment. We have to go back to the last time valuations were this high: the dot-com bubble. It wasn’t 359 days, Bud. It was almost three years.

Bud Kasper: From that perspective. Right.

Dean Barber: There were multiple bear market rallies, which we did a show on here a few weeks ago. Multiple bear market rallies were huge on the upside, 30% and 40% rallies lasted three to five months. Everybody thought, “It’s over.” Then all of a sudden, the shoe drops again, and, boom, it’s on the way back down.

Financial Planning vs. Financial Products

Bud Kasper: Which tells me what, Dean? You got to be paying attention. You have to understand. Most people don’t understand this impact unless they have a full-fledged financial plan. That is how you get uncertainty out of your life to the best of your abilities.

Dean Barber: This is not a product-driven solution. The product salespeople come out of the woodwork during times like this. You’d throw up if everybody listening understood how these product salespeople got paid. You would be sick because they’re not looking for your best interests. They’re looking out for their pocket.

Bud Kasper: They get to use words we don’t get to use because guarantees are in short supply in reality.

Dean Barber: Anyway, get the plan started, and get some clarity and confidence in your life. Start Building Your Plan.

The Stimulus Sugar High and Crash

Dean Barber: Everybody’s blaming the Fed for what’s happening today. The reality is-

Bud Kasper: Oh, I’ve got others to blame.

Dean Barber: Let’s back up. We have been an easy monetary policy since the great recession. And we’ve always said, we don’t know how this will end. And I think we’re beginning to see the early stages of returning our nation to a more normal monetary policy. I have always said you can’t borrow your way into prosperity. And yet the Fed has created more debt in the last three years than … Oh my gosh, it’s just been unreal.

Bud Kasper: I’m going to tell you the evil nature of all this. And I’m going to go back to COVID. And that is politics. When we went into COVID, and we started to realize how severe this disease was and impacting the world. And our answer to that was to stimulate the dickens out of the economy.

We had the fastest retreat in the stock market from February 19th, 2020, to March 30th of 2020th, 35 peak to trough drop at that particular time. They announced that they’re coming in at that time with a three trillion dollar stimulus plan, paying people to stay home and take care of the health conditions if you will, that were warranted they felt at that particular point in time. But we can’t keep doing this to ourselves. We can’t keep feeding the baby the sugar, because you’re going to get a sugar high and then you’re going to get the opposite.

The Duration of Bonds

Bud Kasper: And by the way, it’s not a Democrat vs. Republican thing. Well, it is to a certain extent. But you come back, and you look at what Mr. Biden did. Why was it imperative that he’d go in and shut down the Keystone Pipeline in his first two weeks in office? He wanted to be known as the green president. And I don’t talk about a leprechaun. But in this case, he wanted to emphasize that. And as I’ve said on the show many times, who doesn’t want us to be green? But not stupid about how we get there. And there’s a cause and effect to everything, Dean. And here’s my rationale for that.

Dean Barber: We did a show on the duration of bonds here a few weeks back. And what you said in the last segment, Bud, was that bonds aren’t the ballast to the portfolio they have been over the previous 40 years. And the reason is that we’ve been in a declining interest-rate environment for almost 40 years. There’ve been some blips of upward ticks in the interest rate here and there.

But generally speaking, if you look at the chart going back to the early 1980s and today, you’re going to see a gradually declining interest rate environment. And so, when you look at the duration on a bond, so if you look at the bond aggregate itself, there’s a couple of different ways you can look at that BND or AGG or ticker symbols of ETFs that mirror the bond aggregate, you have an average duration of about 6.7.

Possible Bond Bear Market

Dean Barber: So, a 1% increase in the 10-year Treasury yield will result in a 6.7% decline in the value of BND or AGG bonds. So if you look at BND and AGG, they are now negative this year. Well over 10%. The Fed is hell-bent on raising interest rates to stop inflation, and they’re planning on getting the interest rates on the overnight rate to three and a half percent, and we’re currently sitting below three and a half percent on the 10-year Treasury. I believe there’s a possibility Bud, that that 10-year Treasury, by the end of the year, could well exceed 4% now, maybe even four and a half percent. So does that mean, for the first time in over 40 years, that we could have the bond aggregate enter into the official bear market territory, representing a drop of more than 20%?

Bud Kasper: Yes, sir. It does. It does indeed. And that’s why the Fed Reserve and this is a real problem, folks. The Fed Reserve was forcing money into the stock market to keep interest rates low. So there wasn’t a fixed income option tolerable, especially when you’re getting high, single, low, double-digit returns on the stock market with this fair degree of consistency because of their policy.

14 Years of Fed Forcing Stock Market Investing

Dean Barber: You reminded me of something, Bud. You and I, 14 years ago, sitting right here, in this same studio, were quoting then-Fed Chair Ben Bernanke. And you remember what Ben Bernanke said, “It is the Federal Reserve’s responsibility and duty to get the American public to put their money at risk.” In other words, he wanted to smash interest rates so low that he would force people to invest in the market. And that mentality has been out there for the last 14 years.

Bud Kasper: Yeah. I agree with that statement. And that’s what kind of irritates me with this because it is manipulation. But there’s the high and the low. So we got the sugar high and now we’re getting the sugar low.

Dean Barber: Right. We’re crashing.

Bud Kasper: Yeah.

Strategies to Strengthen Your Financial Plan for Bear Markets

Dean Barber: Look, there are ways to navigate this. And those of you listening to that are clients; you know all the adjustments and things that we’ve done to portfolios this year and the steps that we’ve taken to get more conservative throughout the year. Those of you that are not clients, you haven’t seen it. You may be suffering far more because you’re following a buy-and-hold approach or a simple asset allocation rebalance approach.

Tools to Build Your Own Plan

But we want to help as many people as possible navigate through this. So we’ve done something that we’ve never done before. We’ve opened up our tool to every listener wanting to do this so you can access the industry-leading software that our own CERTIFIED FINANCIAL PLANNER™ professionals use right here in our offices. You can build your plan from the comfort of your own home. This is not a five-minute deal to tell you if you’re okay or not. This is the actual financial planning process. It’s part of our Guided Retirement System.

And so I encourage you to click below if you want to gain clarity and control over your financial life and be able to navigate through these difficult times.

And if you’re saying, “Hey, I don’t want to start building my plan on my own. I’d rather start talking to a CERTIFIED FINANCIAL PLANNER™ right now. I need the help,” click the button below and we’ll get in touch with you.

You’ll see our calendar, and you can schedule a one-to-one consultation with one of our CERTIFIED FINANCIAL PLANNER™ professionals. You can do it virtually, by phone, or we’re happy to meet with you in person.

Bud Kasper: Yeah. And I don’t want this to seem self-serving, but this is a rare opportunity to do this to tiptoe into the reality of accurate financial planning. And it’s not product-driven, folks.

Finding the Right Portfolio for You

Dean Barber: No, no. When you’re building the plan, the last consideration is your asset allocation. Your asset allocation is irrelevant until you create the entire plan. You make a plan first, and then the last piece of it is asset allocation. And when you get to that point, you can design what we call the Goldilocks portfolio. The one that’s just right for your situation can give you that clarity and confidence and put you in control of your financial future. And that’s what it’s all about; that understanding, Bud.

Bud Kasper: Yeah. Challenge us. Go in and do what Dean instructed you to and find out. I think you’ll be impressed.

Dean Barber: Bud, we have many more exciting things to come this year. We’ve got the global unrest, Europe’s rising rates and trouble in China, and all the issues we have here. We’ll keep our finger on the pulse and continue to bring you all the updates on America’s Wealth Management Show. We appreciate you joining us. I’m Dean Barber, along with Bud Kasper. Stay healthy, stay safe. We’ll be back with you next week. Same time, the same place.

Schedule Complimentary Consultation

Click below and select the office you would like to meet with. Then it’s just two simple steps to schedule your complimentary consultation. We can meet in-person, by virtual meeting, or by phone.

Schedule a Complimentary Consultation

Investment advisory services offered through Modern Wealth Management, Inc., an SEC Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management an SEC Registered Investment Advisor. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.