5 Financial Updates for 2023

Key Points – 5 Financial Updates for 2023

- Changes to Social Security Benefits and Medicare

- How 2023 Tax Brackets Compare to 2022 Tax Brackets

- Retirement Plan Contribution Limits Increase

- SECURE 2.0 Changes Required Beginning Date for RMDs

- 6 Minutes to Read

Goodbye 2022 and Hello 2023

2022 is finally in the books. That feels like a long time coming for several reasons. At Modern Wealth Management, we spent a lot of time the past few months preparing for many financial updates for 2023. We’re going to begin the year by reviewing five of the main financial updates for 2023. It’s important to us that you’re aware of these five financial updates for 2023 so that you have clarity and confidence about your retirement as you move forward in this new year. Here’s a quick rundown of the five financial updates for 2023.

- 2023 Social Security Changes

- 2023 Medicare Changes

- 2023 Inflation-Adjusted Federal Income Tax Brackets

- Retirement Account Contribution Limits Changes

- Required Minimum Distributions

1. 2023 Social Security Changes

As the ball dropped in Time Square on New Year’s Eve, the cost-of-living adjustment (COLA) for Social Security recipients sky-rocketed. 2023 Social Security benefits are increasing by 8.7% for 70 million recipients. This comes after a 5.9% increase for 2022 and 1.3% boost for 2021.

The 8.7% bump obviously coincides with highest inflationary levels that we’ve seen in the last 40 years. The early 1980s were a very painful economic period, and we’ve studied it a lot lately to be as prepared as possible for what 2023 could have in store.

This 8.7% COLA increase is the largest boost since 1981 when it was 11.2%. Inflation at that time reached 10.3%. Federal Reserve Chairman Jerome Powell is facing a similar battle that the late Paul Volcker faced with trying to slow inflation. The possibility of Powell closely following Volcker’s playbook of trying to tighten money supply too quickly has spurred recession fears. We went into a recession in the third quarter of 1981. The question now is, how deep of a recession we could go into in 2023? That remains to be seen, but hopefully the 8.7% COLA boost can at least provide some financial reprieve.

Of course, we’ll continue to keep a close eye on the economy to keep you prepared for the possibility of a recession. If you haven’t already, make sure to read our article, 8 Ways to Prepare for a Recession.

2. 2023 Medicare Changes

Let’s continue to look back at the early 1980s as we move on to our second major financial update for 2023: Medicare changes. 2023 marks the first time in 41 years that Medicare Part B premiums fell. That’s thanks in large part the likelihood of changes in expected drug costs.

We were fortunate to have Medicare expert Tom Allen join us again on the Modern Wealth Management Educational Series right as Medicare open enrollment for 2023 was getting underway in October. Tom highlighted how the Medicare B premium is $164.90 in 2023 compared to $170.10 in 2022. Medicare Part B was just one small part of what Tom covered in his ABCs of Medicare webinar. Even though Medicare open enrollment for 2023 ended on December 7, we encourage you to watch the webinar and familiarize yourself with medicare.gov so that you have a good understanding of how Medicare works.

Financial updates for 2023 or any year wouldn’t be complete without touching on Medicare. That’s a big reason why we’re welcoming back Taylor Garner to The Guided Retirement Show for our Season 8 premiere to review changes in Medicare. That podcast will be released on January 17, so don’t miss it!

5 Financial Updates for 2023

on America’s Wealth Management Show

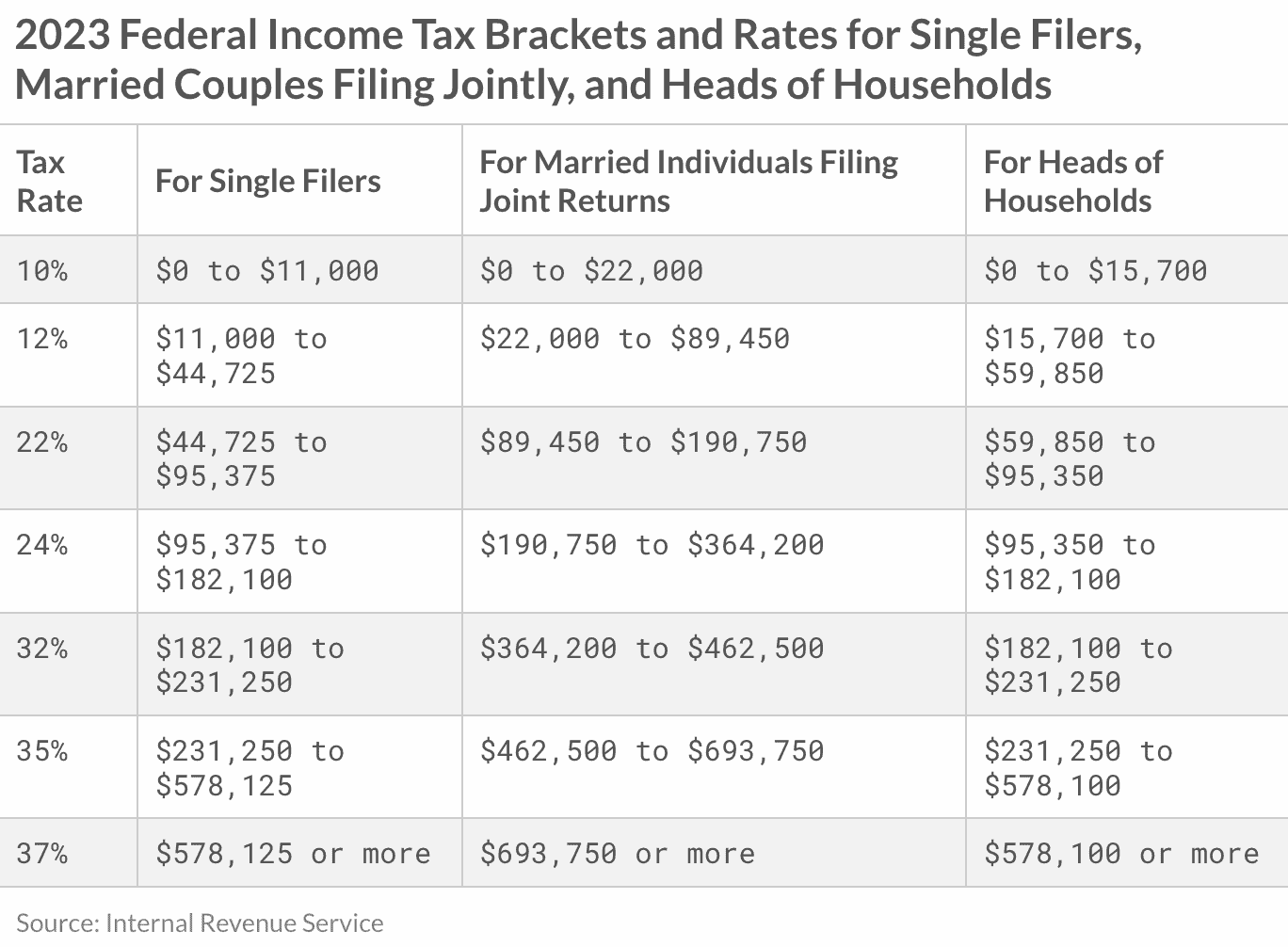

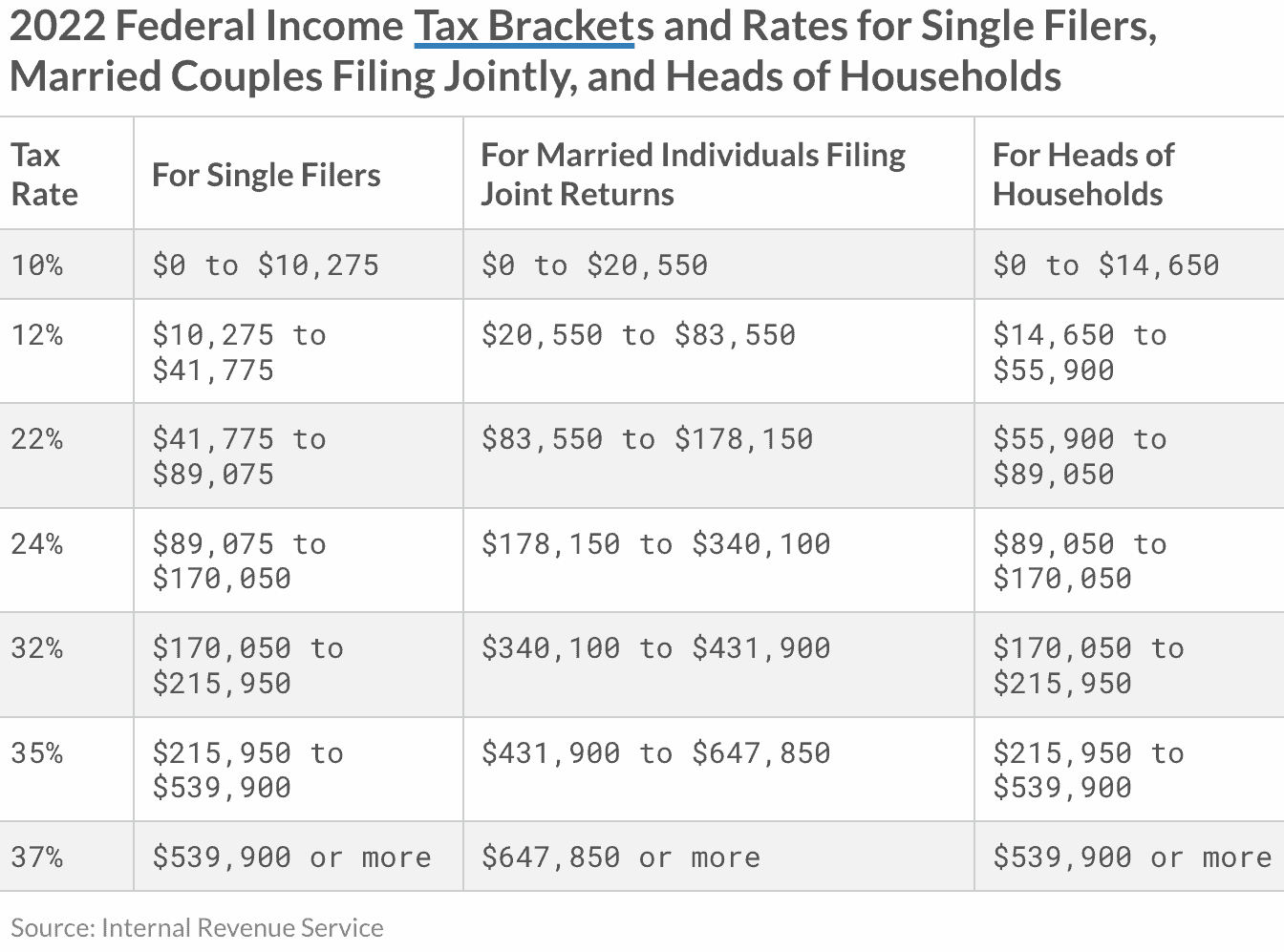

3. 2023 Inflation-Adjusted Federal Income Tax Brackets

Whether we like it or not, inflation is going to have an impact on us on several fronts in 2023. At the end of 2022, we reviewed the 2023 inflation-adjusted federal income tax brackets. This year’s tax brackets come in at No. 3 on our list of important financial updates for 2023.

While tax brackets do scale with inflation, there weren’t substantial changes between the 2022 and 2023 tax brackets. You can compare the brackets from this year and last year below.

FIGURE 1 – 2023 Tax Brackets – Tax Foundation

FIGURE 2 – 2022 Tax Brackets – Tax Foundation

You can see that the tax brackets are bigger for 2023. That can be a good thing for people who have retired and haven’t made significant changes to their monthly budget lately. We met with several people at the end of last year who took advantage of that by doing a larger Roth conversion. The same opportunity could present itself for the remainder of 2023 due in part to the increased brackets.

4. Retirement Account Contribution Limits Changes

The fourth financial update for 2023 should be a welcomed one. Along with tax brackets expanding, retirement plan contribution limits are increasing due to being tied to inflation. The annual contribution limit for traditional and Roth IRAs is going up for the first time since 2019, as it’s increasing to $6,500. That’s a combined $6,500 limit for Roth and traditional, not $6,500 for each.

If you’re 50 or older, a catch-up contribution might have been something you considered last year. If you plan to make a catch-up contribution at the end of 2023, the limit will still be $1,000. Remember that catch-up contributions are an outlier with not correlating to inflation.

Modified Adjusted Gross Income

When it comes to Roth IRA contribution limits, you need to be aware of your modified adjusted gross income. If you’re married filing jointly in 2023, you and your spouse can make a full contribution directly to a Roth IRA if your combined modified adjusted gross income is less than $218,000. You and your spouse can make a partial Roth contribution if it’s between $218,000-$228,000. For single filers, your modified adjusted gross income must be lower than $138,000 to make a full Roth IRA contribution. The range for a partial Roth contribution for single filers is $138,000-$153,000.

If you’re modified adjusted gross income exceeds the $228,000 limit for married filing jointly or $153,000 limit for single filers, it’s still possible to make an indirect Roth contribution via the backdoor Roth IRA strategy.

401(k) and Other Contribution Limits

If you have a 401(k), 403(b), 457 plan (in most cases), or a Thrift Savings Plan, the contribution limit has increased from $20,500 to $22,500. The catch-up provision also increased from $6,500 to $7,500, so you can contribute up to $30,000 following the catch-up.

If you’re a business owner, you probably are curious about the SEP and SIMPLE IRA contribution limits. For SEPs (Simplified Employee Pension plans), you can contribute 25% of your income up to $330,000. A $66,000 contribution would be your maximum contribution. That’s up from $61,000 in 2022. For SIMPLE IRAs, you can contribute up to $15,500 (up to $19,000 with a catch-up provision). That’s up from $14,000 in 2022.

To continue brushing up on retirement account contribution limits and the changes for 2023, make sure to listen to this episode of America’s Wealth Management Show with Dean Barber and Bud Kasper.

5. Another Change with Required Minimum Distributions

We’re going to go into much more detail on our fifth financial update for 2023 in future content, but we’ll touch on it briefly here. Congress did some serious last-minute cramming in 2022, specifically with passing SECURE 2.0.

Trying to stay up to date with the current Required Beginning Date for Required Minimum Distributions the past couple of years hasn’t been easy. It was 70½ for several years. Then, when the SECURE Act passed in December 2019, it changed from 70½ to 72. Now, SECURE 2.0 has pushed it back to 73. If you haven’t started taking RMDs yet, this can be helpful for you. However, if you’ve already started taking RMDs, this unfortunately has no impact on you. You must abide by your current RMD schedule.

So, if you’ve done some tax planning to avoid taking RMDs or paying taxes, this news about SECURE 2.0 probably served as an early Christmas gift. You now have another year in which you can do Roth conversions without RMDs being in the picture.

But all is not merry and bright with the delaying of the required beginning date for RMDs. The delay doesn’t matter for retirees who rely on the funds in their retirement accounts. And if you have been putting off RMDs, the funds in your retirement accounts still must begin to come out when you do turn 73. And the RMDs will most likely be larger because of having a higher account balance.

Again, we’ll be covering the impact SECURE 2.0 could have on you at a much higher level in the weeks to come, so stay tuned.

Keep Up with Financial Updates for 2023 with Our 2023 Retirement Planning Calendar

There is a lot to keep track of just with these five financial updates for 2023 that we’ve outlined. We spent the end of 2022 putting together a 2023 Retirement Planning Calendar so that upcoming financial updates for 2023 won’t sneak up on you. Make sure to download your copy of our 2023 Retirement Planning Calendar below.

2023 Retirement Planning Calendar

Beginning the New Year with a Forward-Looking Financial Plan

We’ve all had moments where we look at a calendar and feel overwhelmed by how much is going on. But just think about how disorganized you can begin to feel without a calendar. We hope that our 2023 Retirement Planning Calendar and all our financial updates for 2023 can give you clarity, confidence, and control in retirement.

As you review our financial updates for 2023, we also hope that it’s evident that everyone should have a financial plan. Our financial planning process is unique to you. Your goals for retirement, expenses, savings, and other assets will be different than your best friends, neighbors, or family members. You can begin building your very own financial plan using our financial planning tool from the comfort of your own home. It’s the same tool that our CFP® professionals use with our clients, and you can access it by clicking the “Start Planning” button below.

And of course, if you have any questions about our financial updates for 2023 or our financial planning process, we want to hear from you. You can schedule a 20-minute “ask anything” session or complimentary consultation with one of our CFP® professionals by clicking here. In the meantime, be on the lookout for more financial updates for 2023 and beyond. It’s our goal to keep you up-to-date on all the things that can impact your retirement as you hopefully enjoy a healthy and prosperous year in 2023.

Schedule a Complimentary Consultation

Click below to get started. We can meet in-person, by virtual meeting, or by phone. Then it’s just two simple steps to schedule a time for your Complimentary Consultation.

Investment advisory services offered through Modern Wealth Management, LLC, an SEC Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management an SEC Registered Investment Adviser. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.