Inflation Expectations for 2023

Key Points – Inflation Expectations for 2023

- The Federal Reserve’s Battle to Stop Inflation

- The Geopolitical Climate

- What’s the Current State of the Housing Market?

- The Future of Interest Rates

- Looking at History to Assess our Current Economic Cycle

- Price-to-Earnings Ratios

- Staying Patient Rather Than Acting on Fear and Greed

- 22 Minutes to Read | 40 Minutes to Listen

A Lot of Questions About Inflation Expectations and Much More Heading into 2023

What is going on with the economy? From inflation expectations for 2023, how high interest rates could go, and the uncertainty within the stock and bond markets, there are so many pertinent questions right now and not many clear answers. David Mitchell of AllianceBernstein joins Dean Barber on the Modern Wealth Management Educational Series to review some of those questions and what they could mean for you.

Having a Financial Planning Is Pivotal

David Mitchell is a regional director at AllianceBernstein and been a featured guest with Dean on The Guided Retirement Show. He has done some extensive research on what’s going on in the economy, interest rates and inflation expectations, and much more. Before David and Dean get into that research and explain the impact it can have on you, there’s an important point they want to make.

“Before you start talking about where to invest your money and what strategies to employ, you need to have a financial plan. With a financial plan in place, you can identify what their money needs to do to accomplish your objectives. Once we know what your money needs to do, we can create the Goldilocks portfolio. From a historical perspective, that will tell us has what’s just right for you with the least amount of risk possible to help you reach your objectives.

Fear and Greed Can Oftentimes Be the Two Biggest Emotions in Investing

A financial plan is always a starting point, and it’s something you can always go back to—especially during uncertain times like we’ve been experiencing in 2022. It helps keep you grounded rather than giving into fear when times are bad or getting greedy when times are good.

“In the absence of knowing what’s enough, the alternative is always wanting more. On my side of the business in asset management, when someone doesn’t know what’s enough, that leads to chasing returns,” David said. “It leads them to be at the whim of the markets because they don’t have a clear picture of how much they need. What’s the intent and purpose of that money? What kind of legacy are they leaving? The financial plan serves as foundational framework.”

If you don’t have a financial plan done, you’re going to be playing a guessing game. And that’s really where fear and greed can really start coming into play. If you have the foundational plan done, you can apply some intellect to the decisions that you make. That helps to remove fear and greed and allows you to make better decisions and get better long-term outcomes.

That makes David think of Daniel Kahneman, who is a behavioral economist who won the Nobel Prize in Economic Sciences.

“As it relates to fear and greed, he stated that fear is a two-and-a-half times the motivator than greed is when it comes to the fear of losing money. Usually, fear is an action that leads to poor outcomes,” David said. “Always keep that in mind. That gets into a lot of our primitive brain. That’s a big deal that Kahneman found in his work.”

Inflation Expectations Continue to Be a Clear Concern

There are quite a few things—some of which we’ve already mentioned—that have a lot of people on edge. The midterm elections have caused a lot of people on both sides of the aisle to be anxious. David works a lot in geopolicy and is a firm believer that geopolitics matters a lot as it relates to markets. However, he thinks this midterm matters a lot less. Here’s why.

“I say that because we’ve had some chatter about the outcome for a few days. But it’s becoming clearer with what is driving that market,” David said. “That’s inflation and the Federal Reserve. Inflation and the Fed will continue to be the market’s main concern.”

Inflation expectations are primarily what the stock and bond markets are going to be trying to figure out in their own way for the next 12 to 18 months. David and Dean both believe that what the Fed is doing right now and inflation expectations for the next 12-18 months supersedes everything else right now in the financial world. Everything else is secondary.

Dean Knows When This Bear Market Will End

Also, remember that Dean made a prediction on America’s Wealth Management Show a few weeks ago that he knows the day that the bear market will end.

“It’s the day that the Federal Reserve says, ‘Inflation is under control. We’re done raising rates,’” Dean said. “And even if the economy is in a recession at that time, I believe that that’s the beginning of the next bull market.”

The Economy and the Stock Market Aren’t the Same

Another important thing to point out when it comes to inflation expectations—among other things—is that the stock market is a discounting mechanism. It moves anticipation of further events.

“It’s happened in every economic cycle that the stock market bottoms before the economy does. The market could bottom and recover while the economy might be in recession. This year, putting inflation aside, the consumer and corporations have done well all things considered.”

However, that’s a big problem for the Fed and the markets. That’s why people need to understand that the economy and the stock market are not the same thing. They’re interconnected, but they are not exact. The market tends to lead the economy as it relates to fundamentals.

A Flashback to the 1970s and 1980s to Help Decipher Inflation Expectations

As we look into the Fed’s battle to stop inflation and assess what inflation expectations should be for 2023, let’s look back at other similar economic cycles. People who were investing back in late 1970s and early 1980s will remember Federal Reserve Chairman Paul Volcker. Volcker was appointed by Jimmy Carter in 1979 and crushed inflation by 1982 by more than doubling the Fed funds rate.

“That was very historic at that time. I think what the Fed is trying to get the Fed funds rate to 5% by March 2023,” David said. “It was at 0%, so that’s a 500% increase. Just from a relative perspective, they are tightening at a much more aggressive pace all things considered than the Volcker Fed did. That’s one reason I think the stock market and especially the bond market have been so challenged this year.”

How High Will the Fed Funds Rate Go?

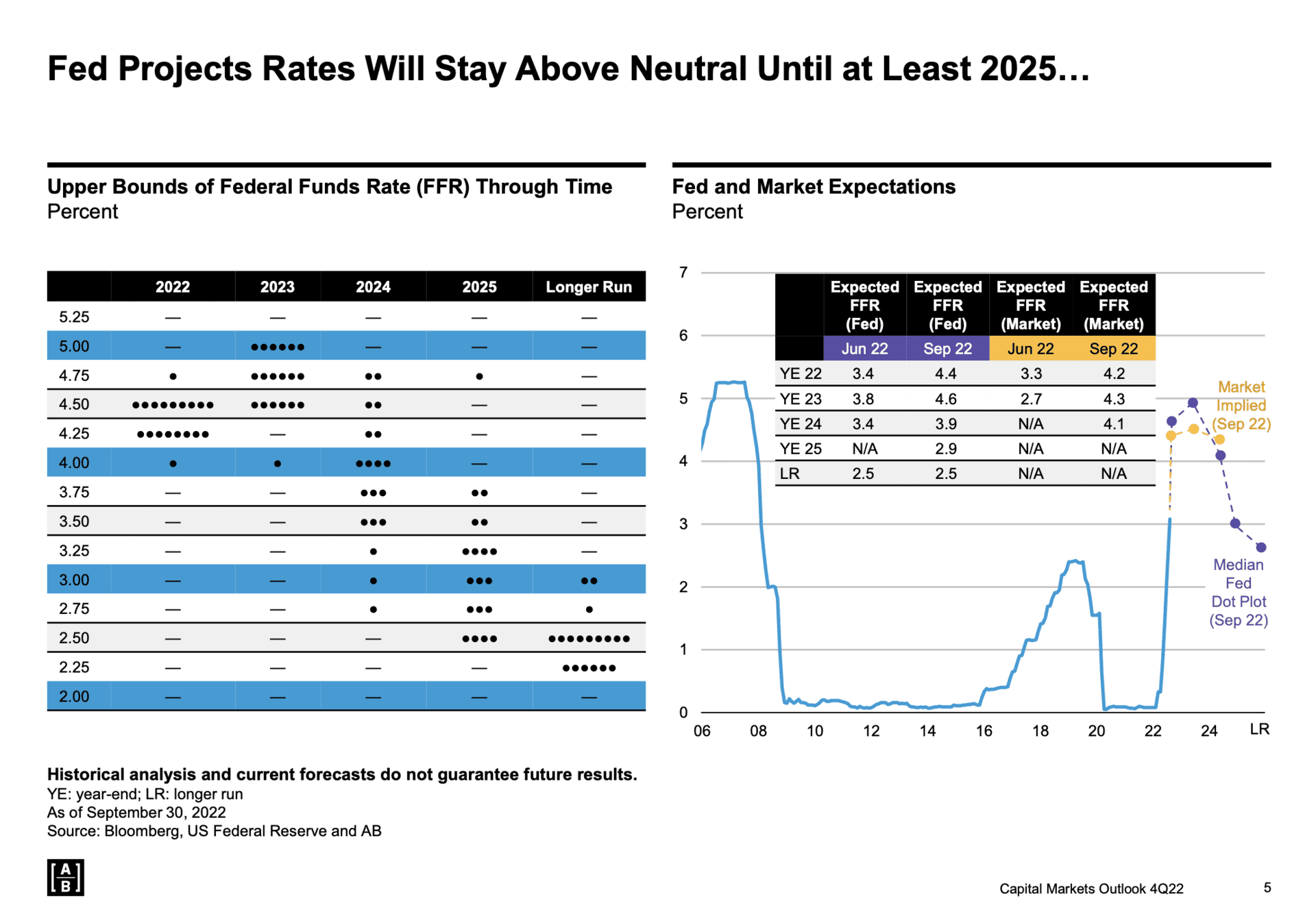

Now, let’s look at the next few years to break down get a better idea about inflation expectations and where the Fed could go from here. To do this, let’s review the Fed’s dot plot below in Figure 1.

FIGURE 1 – Fed Projects Rates Will Stay Above Neutral Until at Least 2025 – AllianceBernstein

The Fed is hoping to get the Fed funds rate to 4.75% or 5% by the March FOMC meeting. But this is where David sees that the Fed and the market are disagreeing a little bit.

“The Fed thinks they’re going to be able stay at that level,” David said. “The Fed doesn’t want to do is get to a level where they think inflation is on its way down in a secular decline and back to less than 3% inflation, but then need to turn around and the economy craters and they need to start cutting rates again. That would look foolish.”

On the other side, David thinks what the Fed is even more afraid of is following the path of Arthur Burns the Fed of the 1970s. They didn’t do enough and had to restart halfway through.

Will the Fed Need to Start Cutting the Fed Funds Rate Before the End of 2023?

The Fed caught is sort of trapped right now. The market is essentially calling the Fed’s bluff. Look at the right side of Figure 1 and what the Fed expects the Fed funds rate to be at the end of 2023 compared to what the market thinks it will be. While the Fed think that the Fed funds rate can hold closer to 4.75%, the market expects that the Fed will need to begin cutting rates before the end of next year.

“The market is saying is that the economy might not be able to stomach that type of policy and maximalist position in this short of time,” David said. “It thinks that the Fed will need to do an about face, which would be probably good for stocks, but very bad for the Fed’s credibility.”

Another Component of the Fed Trying to Temper High Inflation Expectations for 2023—Raising Unemployment

There’s also another reason that the Fed is trapped, though. To truly get inflation under control, the Fed needs to raise unemployment, which is what it’s trying to do—as cruel as that sounds.

“The Fed only has one tool in its toolkit, and that is to crush demand in the economy,” David said. “They can’t fix supply chains or mediate a Russia-Ukraine reconciliation. Their only tool is increasing policy rates and shrinking the balance sheet, which tightens financial conditions and leads to less money in motion, lending and borrowing, and demand.”

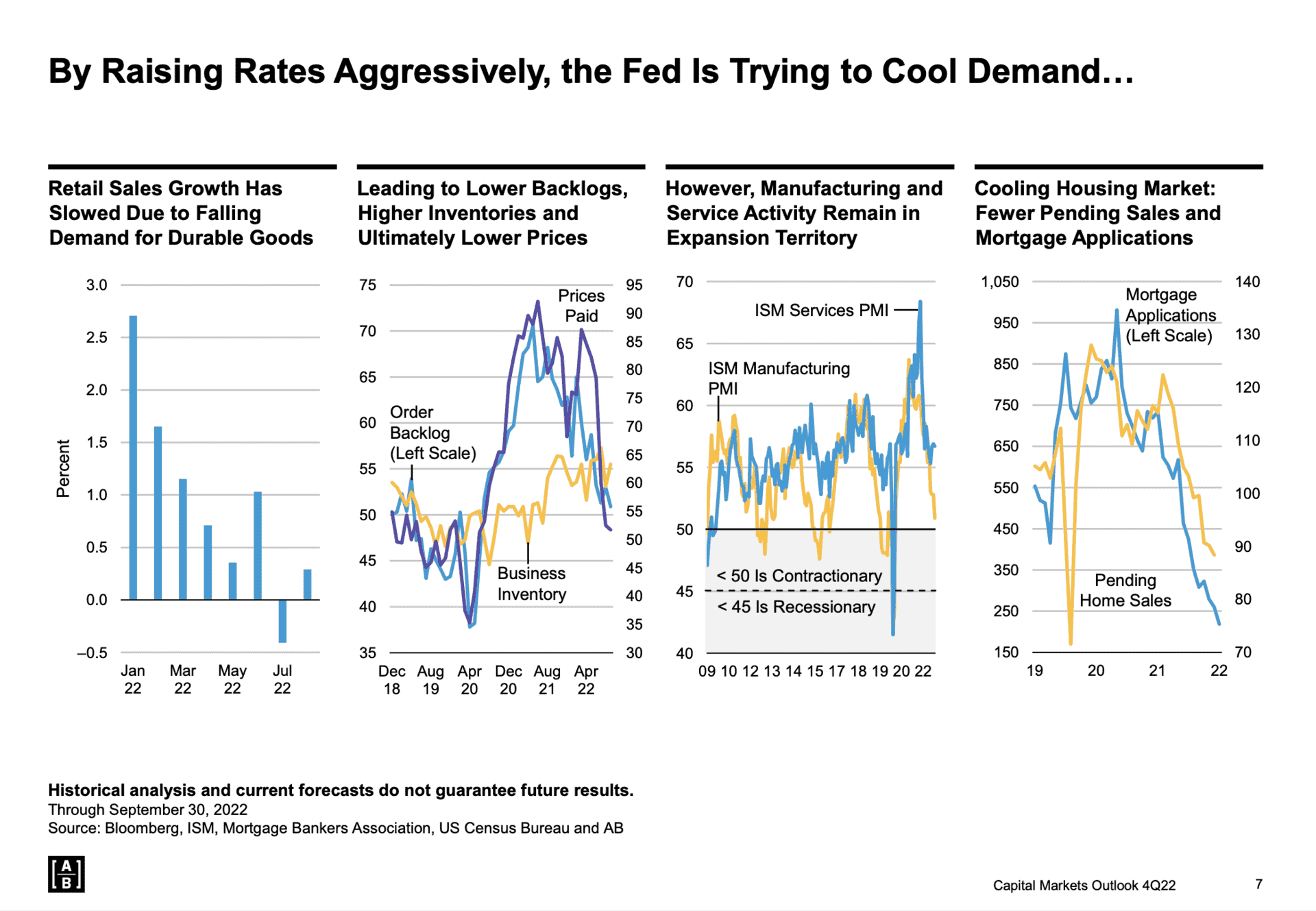

FIGURE 2 – By Raising Rates Aggressively, the Fed Is Trying to Cool Demand … – AllianceBernstein

As you can see above in Figure 2, the Fed is succeeding with that goal. There was a big uptick in people purchasing goods and merchandise through the pandemic. That continued into 2021, but that has now changed. Goods inflation is flatlining now and coming down. That’s evident in what companies are paying for their input cost, especially companies in manufacturing and retail sales.

The ISM Manufacturing Index, which manages the strength of the manufacturing economy through the supply side economy, is going into a contractionary territory.

“Everyone has changed their spending habits from goods to services,” David said. “We’re eating out more and taking more vacations. The services economy is on fire. The Fed wants to get this down over time.”

What’s Going to Happen in the Housing Market?

A big part of the Fed’s quest to crush the economy includes crushing the housing market. We obviously hope it doesn’t come to that. At the same time, we need a place to live, whether you’re buying a home or renting.

“We still have the millennial generation that’s starting to have kids in mass now. With that comes the desire to get out of the apartments and get into a home,” Dean said. “The demand is still there. Although it can bring prices down because of the higher interest rates.”

Affordable Housing Is a Huge Issue

Being able to buy a house is great, but there’s more to it than just the house. You also need the furniture and appliances, which are being impacted by inflation expectations for 2023 in their own right. That’s going to keep that demand up just in the natural sheer force of the number of people that are still looking for their first home.

“The demographics are on the side of housing. We haven’t built enough affordable housing in this country, especially for those younger millennials or Gen Z types that 18 to 30 years old,” David said. “It’s a challenge to afford a house, especially close to where you work. All the jobs are in these metropolitan super centers.”

Now is also not an ideal time to refinance or move. How many existing homeowners are going to swap a locked-in 3% mortgage and move somewhere for a 7% mortgage? They’re not. That’s the problem. They’re not going to move. That’s why the housing prices could hold up well.

What About Rents?

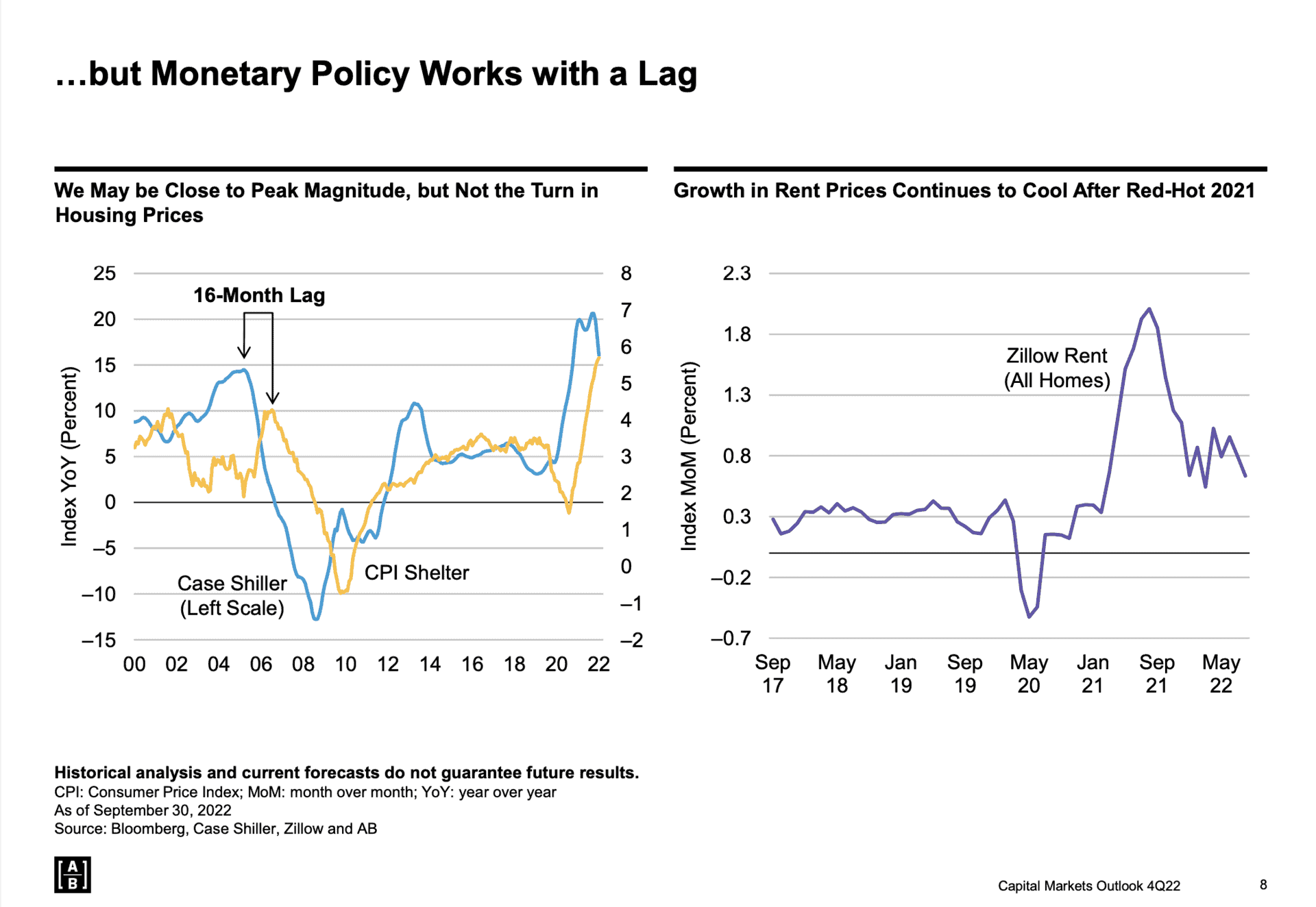

Pending home sales are down. There’s less new construction going on, which is going to keep prices up. The Fed pays attention to the Case-Shiller Index. But the biggest driver of inflation right now on a relative perspective is rents. David has a quick stat for you from the most recent inflation report to help explain why.

“Core inflation, so stripping out food and energy that tend to be more volatile, was at 6.6%. If you had basically 0% growth and rents, that inflation number would come down from 6.6% to 3.9%. It could even get down to 3% if one more variable was added around medical spending.”

Here’s the issue the Fed’s in when it comes to monetary policy that works with rents. Especially regionally, everything about housing and real estate is local. There’s this regionality to it. But rents are universal and the Fed cares a lot about that.

“Rents work on about a 12-to 16-month lag to home prices. If home prices are just now steady and starting to barely come down, it’s going to be another year to year-and-a-half before that manifests to rents and that rent data starts to feed through to the inflation prints.”

The Fed Is Trying to Be Careful with Its Messaging

That’s where the risk is here. What if the Fed keeps going at this pace and doesn’t stop at 5%? The Fed could keep raising rates even higher based upon their rhetoric so far. And the Feds knows how it works with the lag. But how is the Fed going to message that to the public? The Fed knows that rents are going to come down eventually but can’t say that because it doesn’t want to undo all the tightening work that it’s done.

This made Dean think of an interesting question. Are rents going to come down or are they just going to stabilize? Here’s what David thinks about that, and he’ll explain below in Figure 3.

FIGURE 3 – … But Monetary Policy Works with a Lag – AllianceBernstein

“It’s all relative as I always like to say. They’re coming down from a phenomenal growth period in 2021,” David said. “They’ve come down but they’ve come down off crazy highs. Do they come down to negative territory or do they bottom where it’s still growing but relatively speaking a lot less than they were?”

Dean is confident that rents are not going to come back down to the rents we saw two years ago. In other words, you’re not having cheaper rent; you’re just going to have rent that’s not going up as fast.

David’s Perspective on Housing from the Booming City of Nashville

Another variable to add into the housing picture is population growth. David has some unique perspective on this from talking to AllianceBernstein who work at their headquarters in Nashville.

“Nashville had an explosion of population growth. There were a lot of new builds, a lot of multi-family housing, apartments, and beautiful lofts. There are now landlords that are offering a free first month’s rent,” David said. “What does that tell you? That’s a deflationary signal. They are trying to get people into these by offering incentives. Again, it’s very regionally based, but broadly speaking, that’s the issue. And how does that manifest to the headline national data? That’s the big question, too.”

So, other parts of the economy could be slowing and cooling and even in recessionary environment while we’re still seeing increase in rents over the next 12 to 18 months.

The Super-Hot Job Market

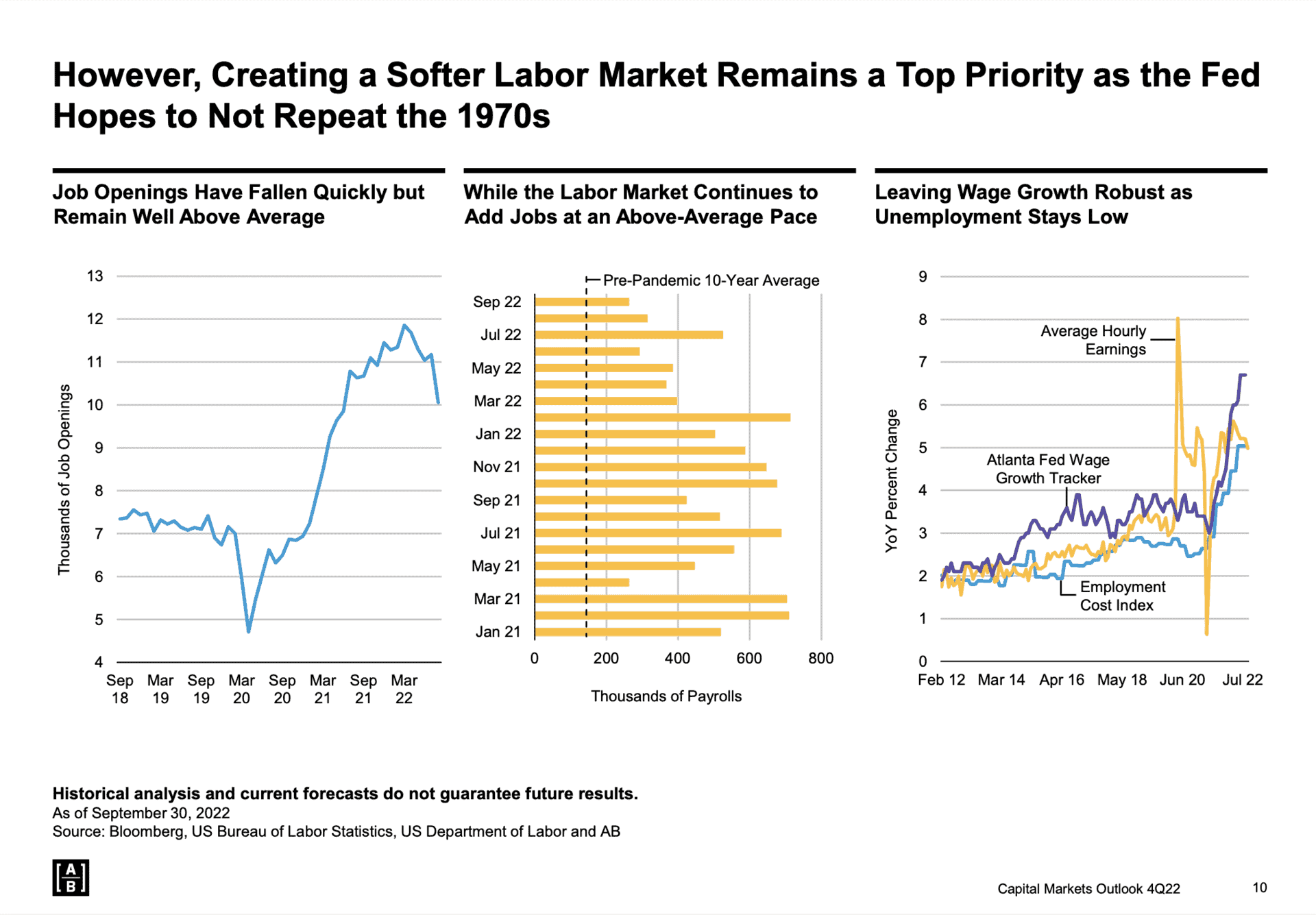

Figure 4, below, also highlights the pickle that the Fed finds itself in with these inflation expectations for 2023.

Coming into this year and for the most part of 2022 has been the greatest job market. Someone that works paycheck to paycheck or in middle management couldn’t ask for a hotter market. There are about two job openings for every job applicant.

“You have a lot of bargaining power as a worker right now—probably the most power in the last 40 years. This has led to phenomenal job growth with net new jobs a month being added back,” David said. “We’ve recovered from the pandemic in this sense. This is just gravy. The unemployment rate went up last month because the labor participation rate picked back up. We added jobs last month with more people coming back into the workforce because they know it’s a really good time as a worker to go in and try to get good wages and good benefits.”

AllianceBernstein’s Base Case for 2023

You might be wondering at this point what AllianceBernstein’s base case for the economy is for 2023. Their base case isn’t very high base, as they put the odds at just over 50% of entering a somewhat mild recession.

“When we say recession, we’re not talking about GDP,” David said. “We’re talking about the labor market and seeing some net job loss by the end of 2023. At some point, the Fed wants the unemployment rate to go up. The Fed explicitly said that. And the Fed think its own research says the unemployment rate needs to go to 4.4% to get inflation under control. That equates to is 1.2 million jobs lost.”

Lots and Lots of Layoffs as the Job Market Cools Off

You don’t need to look any further than Twitter and the jobs Elon Musk has cut there with where this trend is going. As Shane Barber pointed out in his latest housing article, there have been mass layoffs in the real estate industry as well.

“There’s such a benefit right now to being active because there’s so much going under at the micro level of economy within different industries,” David said. “There are sectors that are starting to struggle that are more sensitive to this Fed-tightening cycle. But there are others that had so many tailwinds at their back coming into this economy that are still doing well even though it’s been challenging.”

Job Losses Are What the Fed Wants to See

And as Dean has pointed out on several occasions lately, there are going to be a lot of opportunities born out of all this chaos. Just look at the state of the union coming into next year and why David thinks a recession is likely. He thinks that the unemployment rate will tick up at some point we’re going to start seeing monthly job losses.

“How is the Fed going to react if we’re having 150,000 to 200,000 jobs lost a month? Are they really going to be still tightening policy?” David said. “What would they need to see to pivot? I think it’s going to be hard for them to continue to increase if we’re seeing job losses to that extent, but I digress.”

But again, as cruel as it sounds, that’s what they want to see as they try to stop inflation. Their No. 1 goal is to lower these inflation expectations in 2023. The thing is that the Fed has blinked before.

“The Powell Fed has not been a very good Fed at predicting. Predicting the future is hard and we all know that,” David said. “It’s probably more luck than skill oftentimes with predicting the next six to 12 months. But they’ve made a couple mistakes already. I’m just very curious to see what happens when the economy does materially weaken.”

What Should Our Inflation Expectations Be for 2023?

So, does the Fed stay the course to get inflation back down to 2%? Or will it be OK with having inflation around 3%? What should inflation expectations be for 2023?

Like we mentioned earlier, the Fed doesn’t want to make the same mistakes that were made back in the late 1970s. The Fed doesn’t want to say that they’ve crushed inflation, lay off or pull back a little bit, and then have it come back with even stronger force. That’s what happened in the early 1980s and the Fed doesn’t want to have the same inflation expectations going into 2023. This is even evidenced by how often Jerome Powell cites Paul Volcker.

“Powell said he’d rather go too far than not far enough,” Dean said. “To me, inflation is the silent killer. Inflation doesn’t cause people to go broke, but it’ll cause people to live like they’re broke.”

Reining in Inflation

Inflation is very emotional. It’s very behavioral. If we think something is going to be more expensive four months from now, what do we do today? We go out and buy it because we don’t want to pay more in the future, which contributes further to inflation today.

“The Fed looks at inflation expectations. Powell often talks about wanting inflation expectations to stay anchored, to stay low,” David said. “Because if the market and consumers suddenly start to believe inflation is going to be higher one to five years out, they start to ramp up more spending today. That’s what he is terrified of.”

When we talk about Powell’s rhetoric of channeling his inner Paul Volcker, inflation expectations have stayed low all things considered. One-year inflation has come from a high of 4.1% just a couple months ago down to 2.9%. What Powell is saying is working. The question is, will he perform as advertised when it’s crunch time? We don’t know, but rather than wait and see and play a guessing game with inflation expectations for 2023, we encourage you to read our article, 10 Ways to Fight Inflation in Retirement.

Stock Expectations for 2023

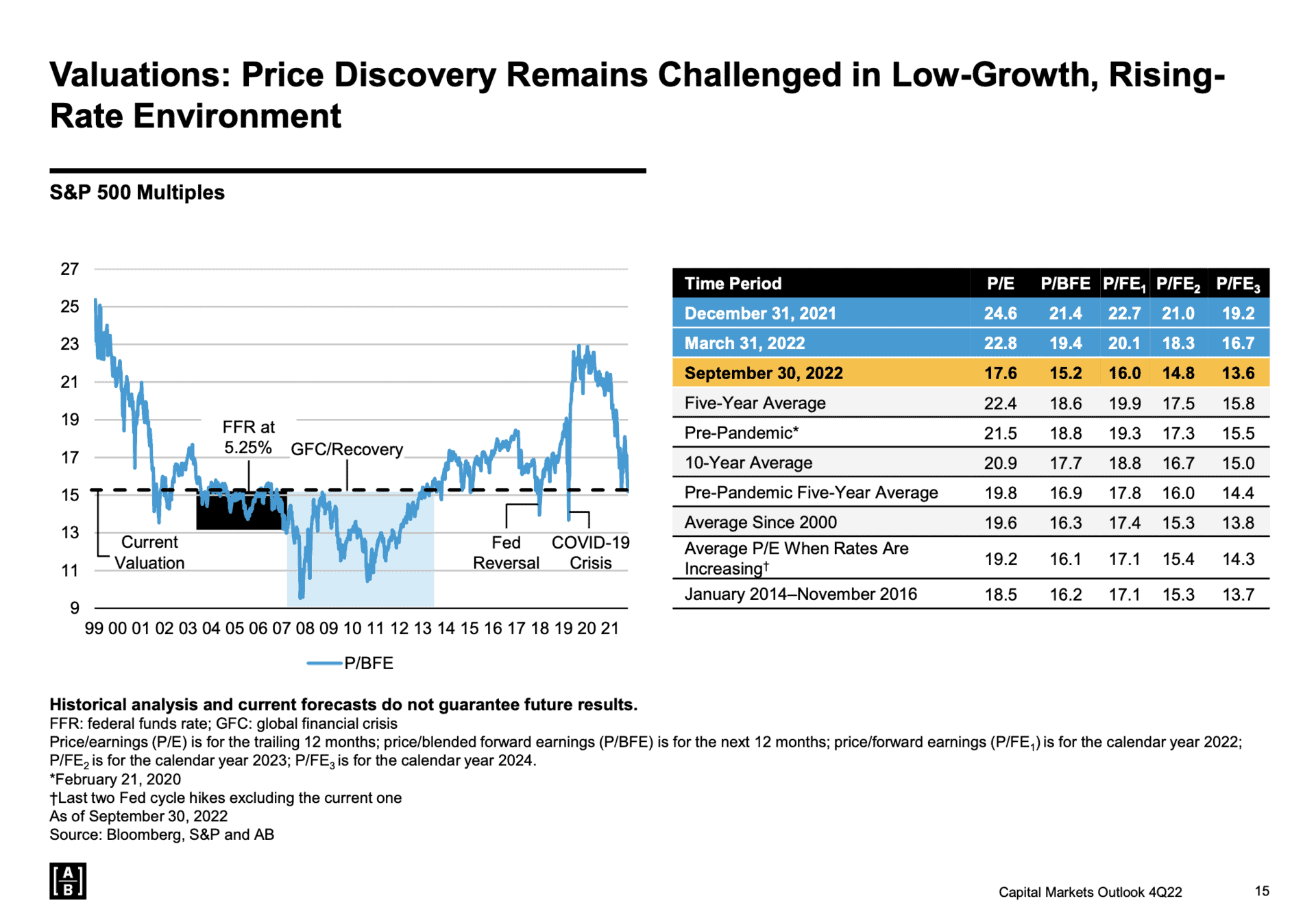

As we continue to discuss inflation expectations for 2023, it bears asking what all this means for stocks. One thing that we can control is the price at which we buy something. We’ll dive into this below in Figure 5.

“What’s interesting about stocks though is that people don’t often like to buy stocks when they’re on sale because it tends to be a period of a lot of fear and uncertainty. Just look at the trailing price-to-earnings,” David said. “Markets were the most expensive they’ve been this century coming into this year with price-to-earnings at 24.6. The good and bad of it is that was a rocky road to get to this September.”

Markets are around 20%, but because it’s largely been on the price side, the earnings of companies have been amazingly resilient through this. If earnings hold and we don’t go into an earnings recession, stocks look cheap at 17.6 times trailing earnings. The earnings are even cheaper if you’re trying to discount future cash flows.

Are Stocks Fairly Valued Right Now?

From purely a price standpoint, if you’re investing for more than a year or two, today looks to be an attractive time to buy good companies. But if you’re asking for clarification if stocks are fairly valued right now, David says it depends on what the price and the earnings are. If earnings decline, then the P/E ratio could go right back up. But does it go up enough to justify the market not being down another 10% or 15%?

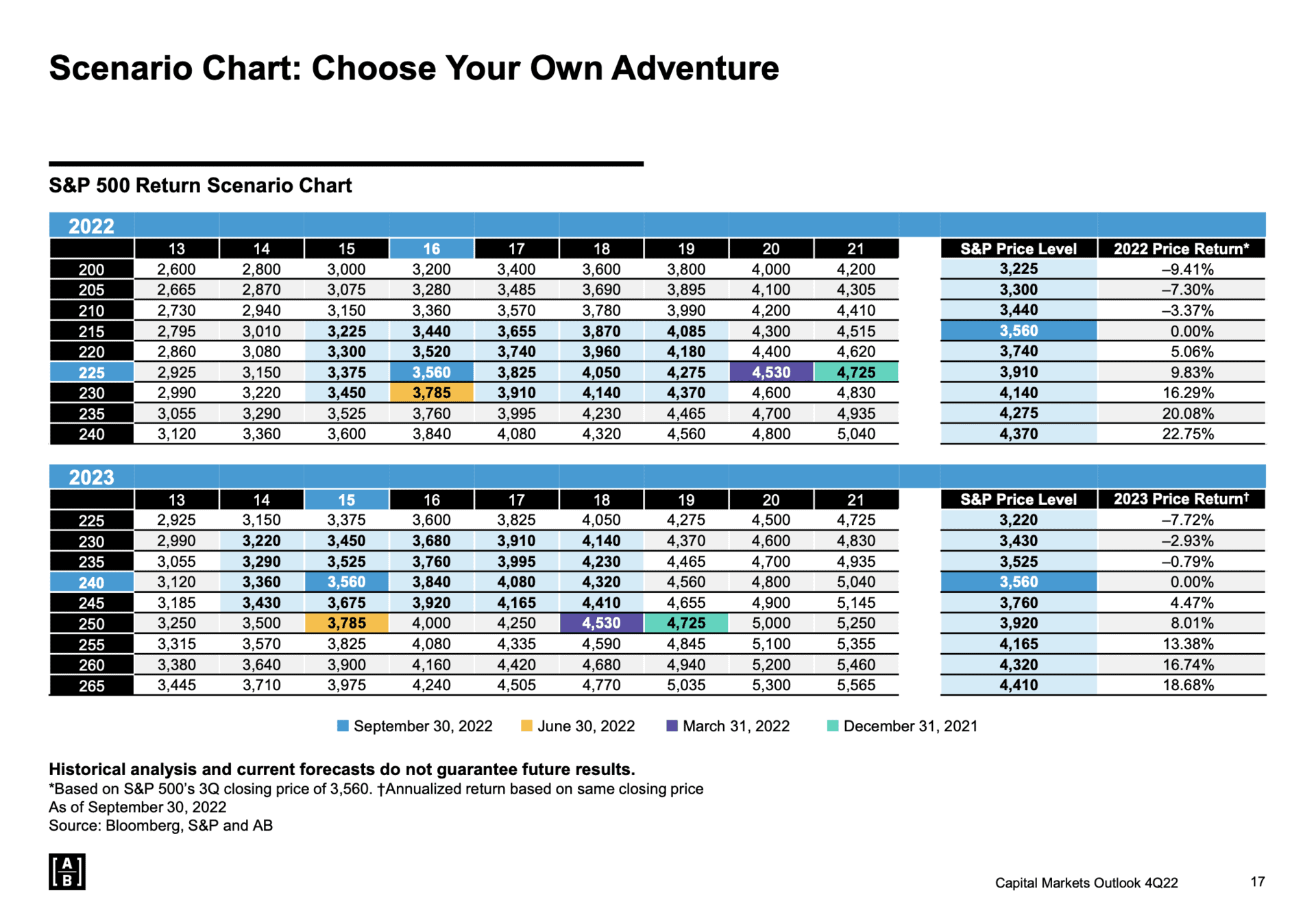

This brings us to Figure 6. It looks very busy when you first look at it, but it’s actually very simple and helps people pre-experience what the next year to year-and-a-half could look like.

FIGURE 6 – Scenario Chart: Choose Your Own Adventure – AllianceBernstein

“We’re showing what the S&P 500 level would be based upon what the price is, the P/E multiple, and where earnings come into. For example, let’s just take this year right now,” David said. “If today was December 31 and all the earnings reports were in for the year, we think earnings per share for the S&P 500 is going to be between 220 and 225. The market assigned about a 16 multiple to that, which gets us into the 3,700 to 3,800 level. So, for 2022, the market looks pretty fairly valued.”

What’s different about the beginning of the year is that the asymmetry from a return standpoint is to the upside. So, let’s say that things do get a little better, inflation comes down a little faster, and that the fundamentals in the economy don’t fall apart. To get back to 4,400, you’re looking at 20% returns versus the downside. Now, if earnings decline this year or next, the downside is a little more capped. It’s all about beginning and endpoint sensitivity.

Looking Ahead to 2023

Now, let’s look at next year. If earnings come in at 225 this year, what if we have zero earnings growth next year? If we have an economic recession, that could be possible. Companies could hold the fort if they can’t grow earnings. What would that look like?

Go back to Figure 6 and go to 225 again and assign a 15 multiple to that. That gets you to 3375. There’d be a little more downside to go. Here’s the way Dean sees it, though. If we get to 240 in earnings in 2023 and the markets stay in that 15 to 16 multiple, you’re a flat market or a slightly positive market for 2023. This would lead a person to believe that there is more upside potential than downside risk.

What Happens to the Price to Earnings If We Have a Recession?

From just evaluation standpoint, looking at price relative to earnings, David agrees. But there’s a big wild card. If we have a recession, what happens to both the P and E?

“When you hit max capitulation in the markets, we have those crazy swings where the VIX goes over 40 and there’s a tons of volatility, usually the P/E goes to about 14, depending upon what interest rates are doing,” David said.

But what if earnings decline next year? That would be the case for testing 3,100 or 3,200.

“There are strategists on Wall Street at the big investment bank saying, ‘We need to test that,’” David said. “That’s the cathartic level where you’re going to find a bottom because markets need to price in some earnings. That’d be about another 15%. Worst case scenario.”

A Mild Recession in 2023?

When all is said and done, David believes we’ll experience a recession in 2023, but he thinks it will be a mild one. This is still new territory here, though, because of how the pandemic shortened the business cycle.

“We have these long cycles. Companies at the end of it are trying to manufacture their earnings,” David said. “They use a lot more leverage to juice their earnings. But companies couldn’t do that this time.”

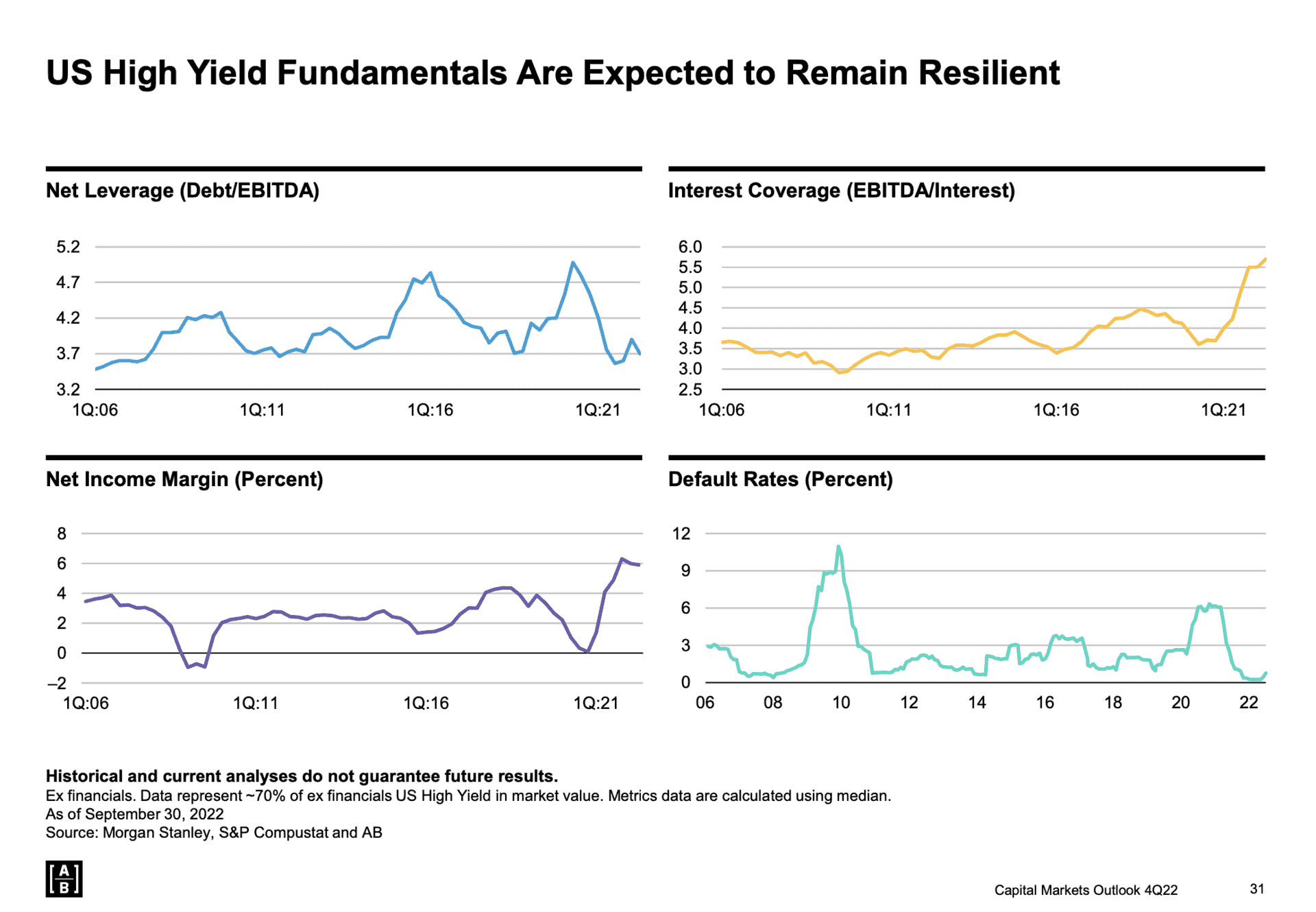

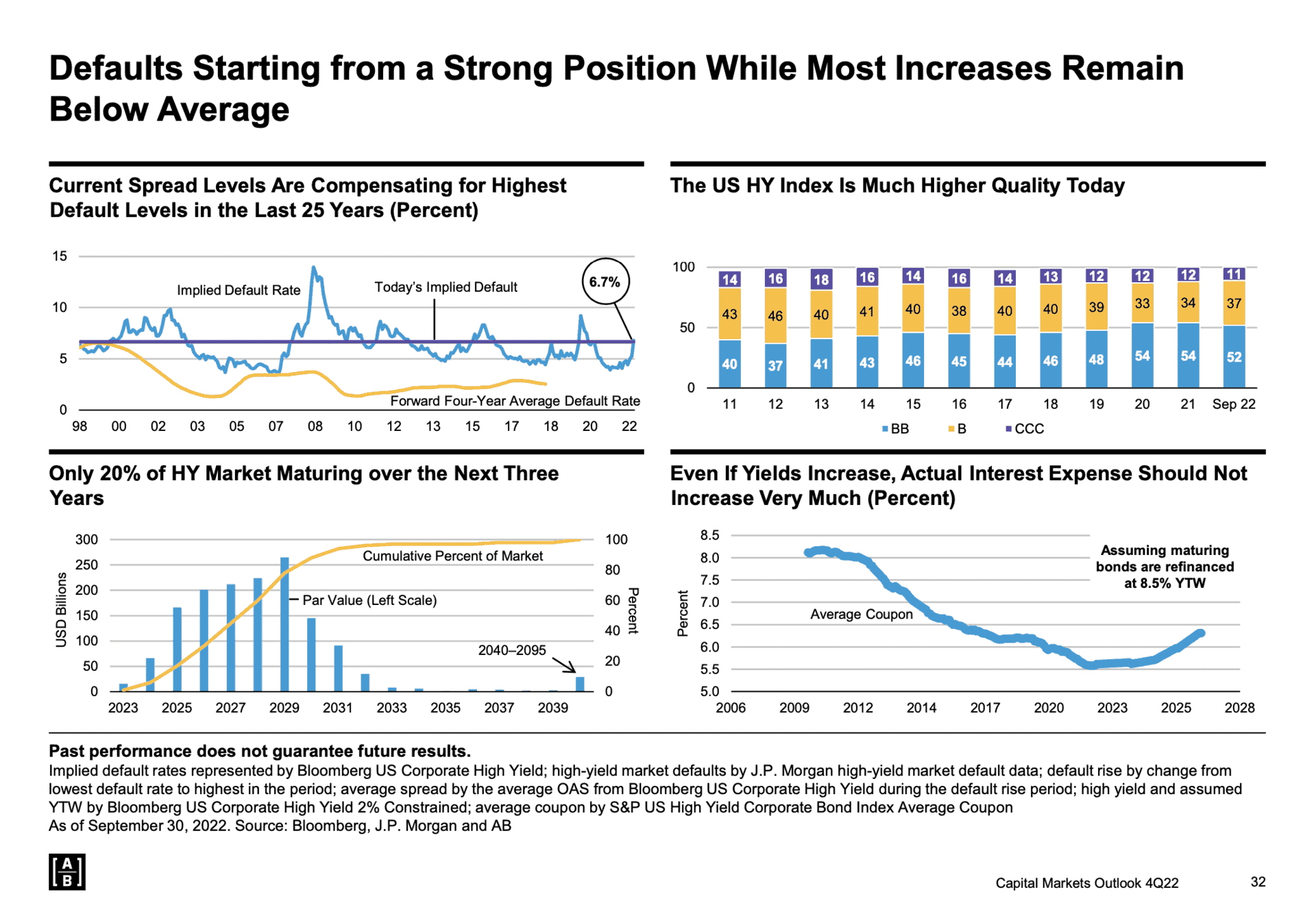

That brings us to Figure 7, where we look at the corporate credit market and U.S. high-yield bonds. Those are just the bonds from a lot of corporate companies.

FIGURE 7 – US High Yield Fundamentals Are Expected to Remain Resilient – AllianceBernstein

“These are companies that might not have pristine fortress balance sheets. They’re all in really good shape,” David said. “They didn’t have time to do what they typically do, which is push a little too far, too fast, and get themselves into trouble. They should be able to withstand a moderate recession better than maybe they did in prior business cycles.”

Back to Fear and Greed

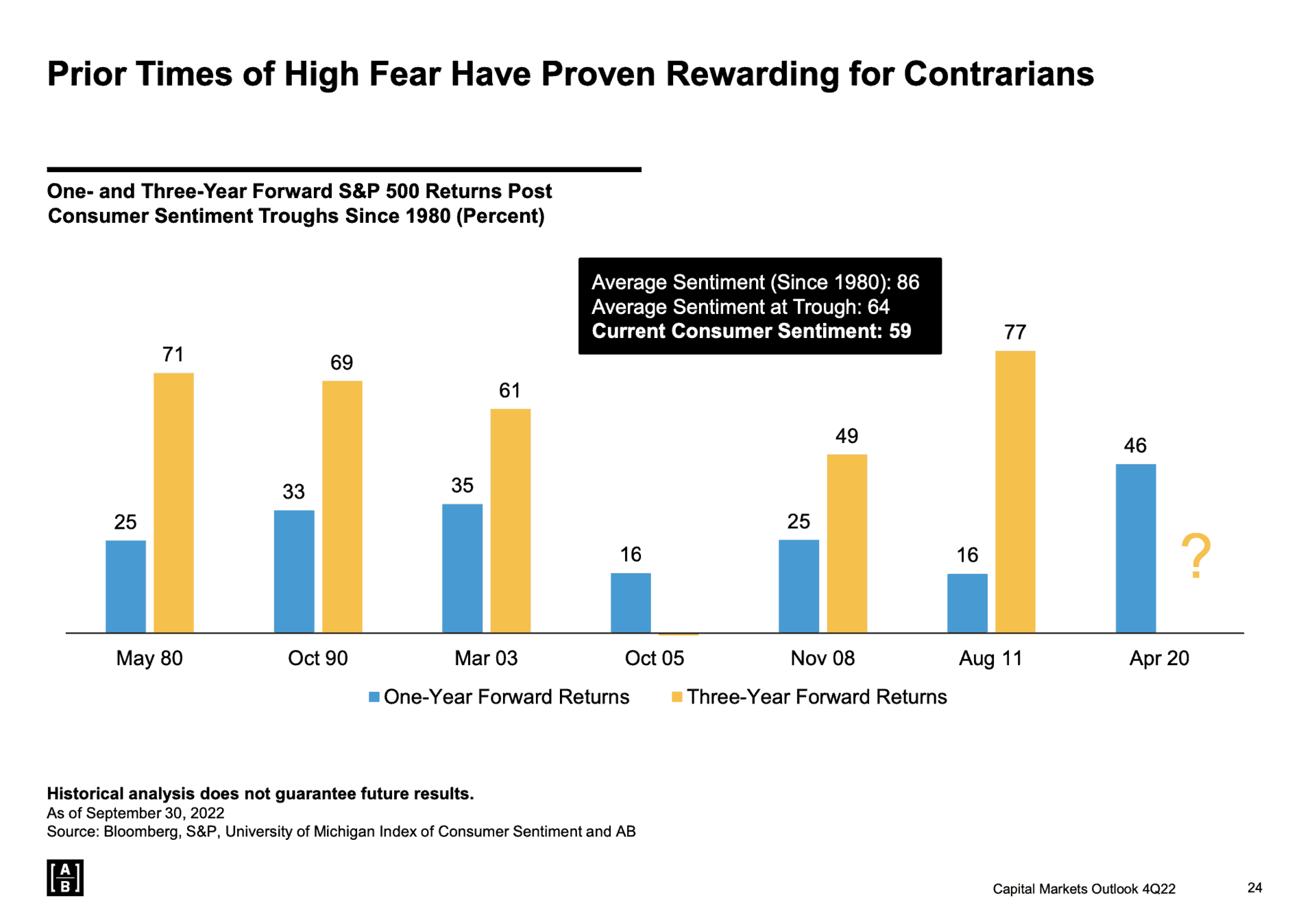

Now, let’s shift our attention to Figure 8 below. It gives a good barometer for just how to think about fear and greed like we discussed earlier.

FIGURE 8 – Prior Times of High Fear Have Proven Rewarding for Contrarians – AllianceBernstein

As Warren Buffett said, “Be fearful when other are greedy and greedy when others are fearful.” This is more the former. What we’re showing here is going back to Paul Volcker and we talked about from the early 1980s.

“This is another great indication about how the stock market tends to be a discounting mechanism,” David said. “It looks out and finds a bottom before the rest of the economy and average person realizes it’s happening.”

Looking Back at History Again

Figure 8 shows the trough in consumers. It’s using the Michigan survey, which is of the gold standard of consumer sentiment. The average trough since 1980 is 64. We’re at 59 in last report, which helps highlight why people are so pessimistic about outlook for the economy in 2023 to go along with inflation expectations.

In Figure 8, we’re showing cycles of consumer sentiment bottom. Lower is worse. And we’re showing the one-and three-year returns going out on the S&P 500.

Forward-Looking Financial Planning Is Pivotal

May 1980 was when the consumer sentiment troughed in that cycle. If you were to buy that month, your forward one-year return for the S&P 500 was up 25%. Your total three-year return was 71%. People might be wondering why consumer sentiment was so low in October 2005 and then why was the three-year return was so bad? Well, that’s because it hit 2008 amid Lehman Brothers collapsing.

“That’s an anomaly. Not to say it couldn’t happen again, but the bottom line is that we do think that if you’re able to use this as a guide to see how much fear and pessimism is out there,” David said. “It’s being able to say, ‘I don’t need my money. I have a plan. I have all the cash I need for the next year or two. I’m thinking about the next two, three, four, five years out.’”

Dean points out that if we could extrapolate to April 2023, we’re at a 29% three-year number on the S&P 500 when doing a three-year lookback. And again, April 2020 was the beginning of the pandemic, which is why pessimism was so high.

“You saw the one-year return. We know how it ended,” David said. “The three-year return is still positive. I think people are off their high watermark. Their portfolios were at a certain value and now they’re down 15%, 20%.”

October 2008 Was a Time We’d Like to Forget

It’s not very often that you had to get a peak in the market right at the end of a calendar year. That was a little different. But fast forward to September 2022. We’re at a bearish point with consumer sentiment. That makes Dean raise another question. What was the lowest that it ever got—knowing we’re at 59 now and the average trough was 64?

“It was a little lower than 59 in October 2008, but not by a ton. That was hopefully once-in-a-career type of event with a true financial systemic crisis,” David said. “That is not in our base case today as a likely scenario. It feels worse today. All this is because inflation and inflation expectations. With the Financial Crisis, we had a crisis in the mortgage market and it manifested and spilled over into the securitization of mortgages and subprime.”

Comparing Consumer Sentiment Today to 2008

David points out that when you’re paying more for food, gas, etc., inflation just gets in your psyche a bit more. That’s why inflation is a tough economic variable to account for. But like Dean said, sentiment today is on a similar level as it was in the Financial Crisis. Could we go lower? Yes, but it would need to be a nasty recession for things to get a lot worse.

“In November 2008, if that’s when the sentiment bottomed, the market had another four months of horrific returns,” Dean said. “That went through December, January, and February until it finally bottomed out in mid-March 2009.”

Consumer sentiment also bottomed out around the same time. But that wasn’t exactly a time when people were trying to load up on stocks. They were scared.

The Corporate Bond Market Is in Bear Market Territory

As we conclude our discussion on inflation expectations for 2023 and the future of the markets, there’s a phenomenon that Dean and David have never witnessed until now that they’d like to talk about. That phenomenon is the corporate bond market being in bear market territory.

If you look at TLT, which is a 20-year treasury, it’s down 36% on the year. The bond aggregate is down 18% over the last 12 months. With the stock market, the official term of a bear market is when you’ve fallen 20% from a previous high. Well, if the Fed continues to raise rates, could we see a decline in fixed income that will exceed 20% and put us into an official bear market.

“Bonds are mathematical contracts. There’s less guesswork in bonds than there are in stocks,” David said. “I talked about stocks being forward-looking indicator in a discounting mechanism, but the bond market’s even better at finding bottoms. If you look at the 10-or 20-year treasury, it tends to peak at about six months before the Fed is done tightening.”

Are We Nearing the End of This Bond Bear Market?

A lot of people say the bond market is where the smart money is, especially if they’re a bond person. They would say that the market tends to know where the economy is going better than the Fed does.

“The Fed tends to be late to the party. We think we’re probably in the eighth or ninth inning of this bond bear market,” David said. “We’re seeing some stabilization in yields. If you were to ask me to pick pound for pound on a risk-adjusted basis what asset class is going to do best in the next 12 months, I would probably tell you corporate credit. You can buy high-yield bonds today with a starting yield of 10% or more. That’s an interesting proposition.”

Default Cycles

That puts those bonds around an 83-86% discount. If you look at today with that sort of average price, there are spreads that measure the risk of buying a corporate bond over a treasury bond. That’s forecasts a four-year default cycle of around 5-6% a year. Let’s look at defaults below in Figure 9.

“The closest we came to that was the Dot-Com Bubble because there were so many bankruptcies, which is a lot of just shoddy companies. But we didn’t even hit that in the Financial Crisis over a four-year period,” David said. “Relatively speaking, the bond market has experienced a lot more pain than the stock market because bonds shouldn’t go down this much. The engine of a bond’s return is cash flow. It’s interest income. If I know that I’m guaranteed to collect 10% in the next 12 months, can wait this out somewhere, and still earn a good return that above inflation, corporate bonds are pound for pound the asset class pick for the next 12 months.”

There’s some securitization involved as well. To Dean’s point about rents, David is intrigued by a lot of the residential housing-related bonds. Some mortgage-backed securities are trading at 20-30% discounts. They’re turning in at 75% as opposed to 80%.

“There’s a lot of good deals out there, but again you need to do the planning,” David said. “You can’t just blindly buy a high-yield bond index. Because for other times, those indexes aren’t ideal with the way they’re constructed. That’s why you should have a steady hand with a portfolio manager that’s been looking at these sort of corporate bonds for 20, 30, 40 years and knows what they’re doing.”

Planning Around Inflation Expectations for 2023

David and Dean went through a lot of information about inflation expectations, the current state and future of the markets, and much more. So, if you have questions about what Dean and David review, please reach out to us. The important takeaway from this is that if you’re looking into investing and don’t have a financial plan, you’re just doing guesswork. A financial plan can give you clarity and confidence with your investments, and it covers so many more aspects of your financial life that are more important than your investments.

You can begin building your financial plan by using our industry-leading financial planning tool at no cost or obligation. Just click the “Start Planning” button below to begin building your plan from the comfort of your own home.

We hope that you’ll realize when using our tool that it’s imperative to account for inflation in your plan. Times like we’re going through right now are proving why that is a must. By scheduling a 20-minute “ask anything” session or complimentary consultation with one of our CERTIFIED FINANCIAL PLANNER™ professionals, you can ask us questions about inflation expectations for 2023 and other things that apply to your unique financial situation.

Stay Tuned for an Update from David in 2023

We want to thank you for tuning into this Modern Wealth Management Educational Series webinar about inflation expectations. And we want to thank David for providing his keen insight. Be on the lookout in 2023 for David to be joining us on our podcast, The Guided Retirement Show, to provide an update and another detailed economic outlook.

Schedule Complimentary Consultation

Select the office you would like to meet with. We can meet in-person, by virtual meeting, or by phone. Then it’s just two simple steps to schedule a time for your Complimentary Consultation.

Lenexa Office Lee’s Summit Office North Kansas City Office

Investment advisory services offered through Modern Wealth Management, LLC, an SEC Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management an SEC Registered Investment Adviser. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.