Tax Rates Sunset in 2026 and Why That Matters

Key Points – Tax Rates Sunset in 2026 and Why That Matters

- Tax Rates Are Going Up After 2025

- Comparing the Current Tax Brackets of the Tax Cuts and Jobs Act to the Ones of 2017 (That’s What We’re Going Back to in 2026)

- Yet Another Reason to Consider Roth Conversions

- It’s All About Paying the Least Amount in Taxes Over Your Lifetime, Not in a Single Year

- 7 Minutes to Read

Going Back to Tax Rates of 2017

Last fall, we published an article titled, What If We Go Back to Old Tax Rates? By old tax rates, we’re talking about the tax rates from 2017 that were in place prior to the Tax Cuts and Jobs Act. Well, the tax rates from the TCJA are still scheduled to sunset in 2026, so that what-if scenario we discussed a year ago is looking more and more likely.

While 2026 might seem like it’s way down the road, there’s a reason why we focus so much on tax planning at Modern Wealth Management. As we look at the tax rates of 2022 and what they’re projected to be in 2026 (the same rates from 2017), you’ll see why the time to act is now.

Before we break down the numbers of the tax rates sunsetting in 2026 and why that matters for you, we encourage you to take the information we’re about to share and go one step further by utilizing our industry-leading financial planning tool. By clicking the “Start Planning” button below, you can begin building your financial plan with the same financial planning tool that our CFP® Professionals use.

Tax Rates Are About to Go Up

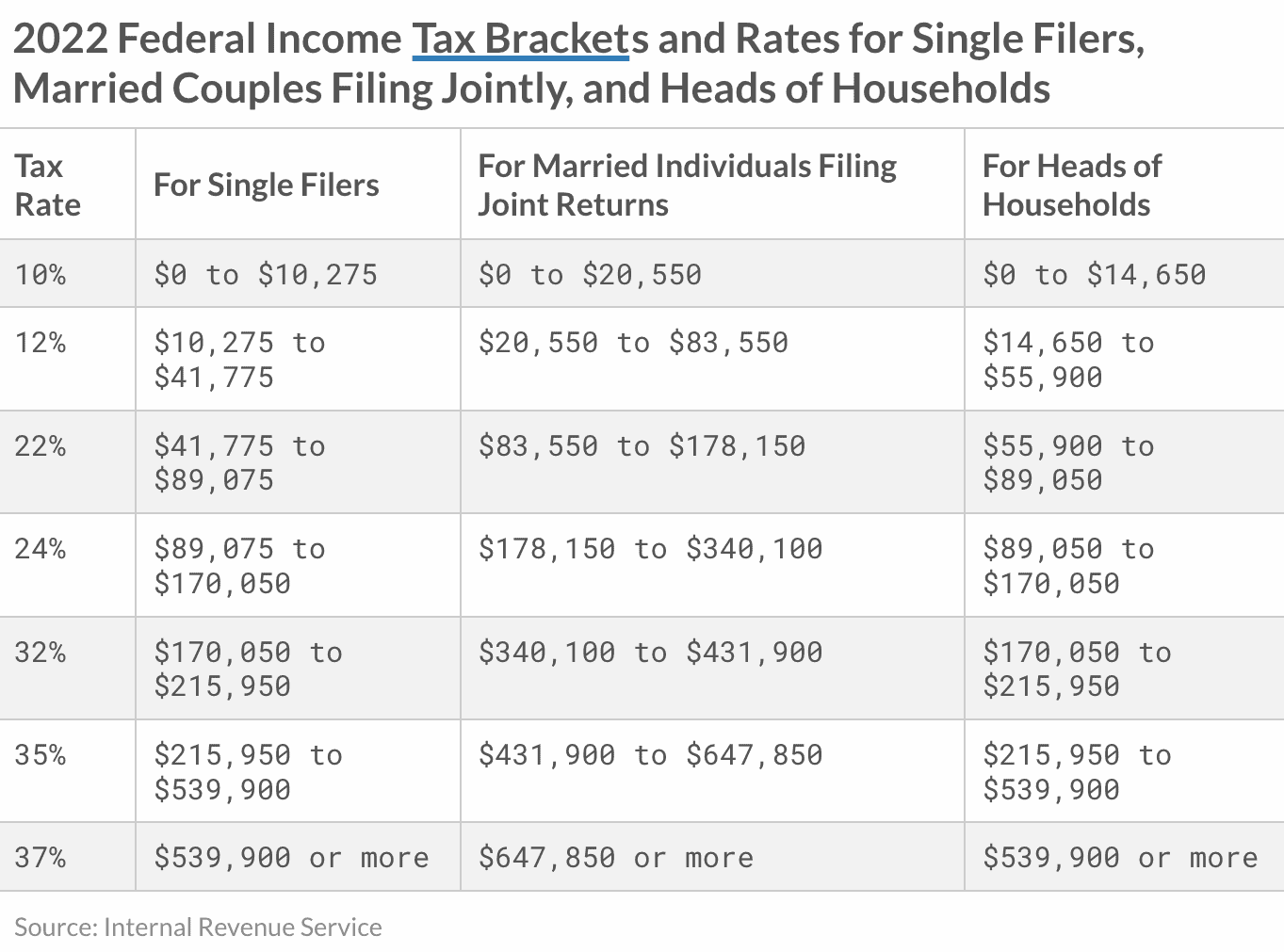

The simple answer to why tax rates sunsetting in 2026 matters for you is that all tax rates will be going up. With tax rates rising, your net income will likely decline. While we can only hope that inflation will be in check again by 2026, an inflationary environment would no doubt make matters that much worse. Let’s look at the 2017 and 2022 tax brackets to see what bracket you would fall into in 2026. First, Figure 1 shows the current tax brackets.

FIGURE 1 – 2022 Tax Brackets – Tax Foundation

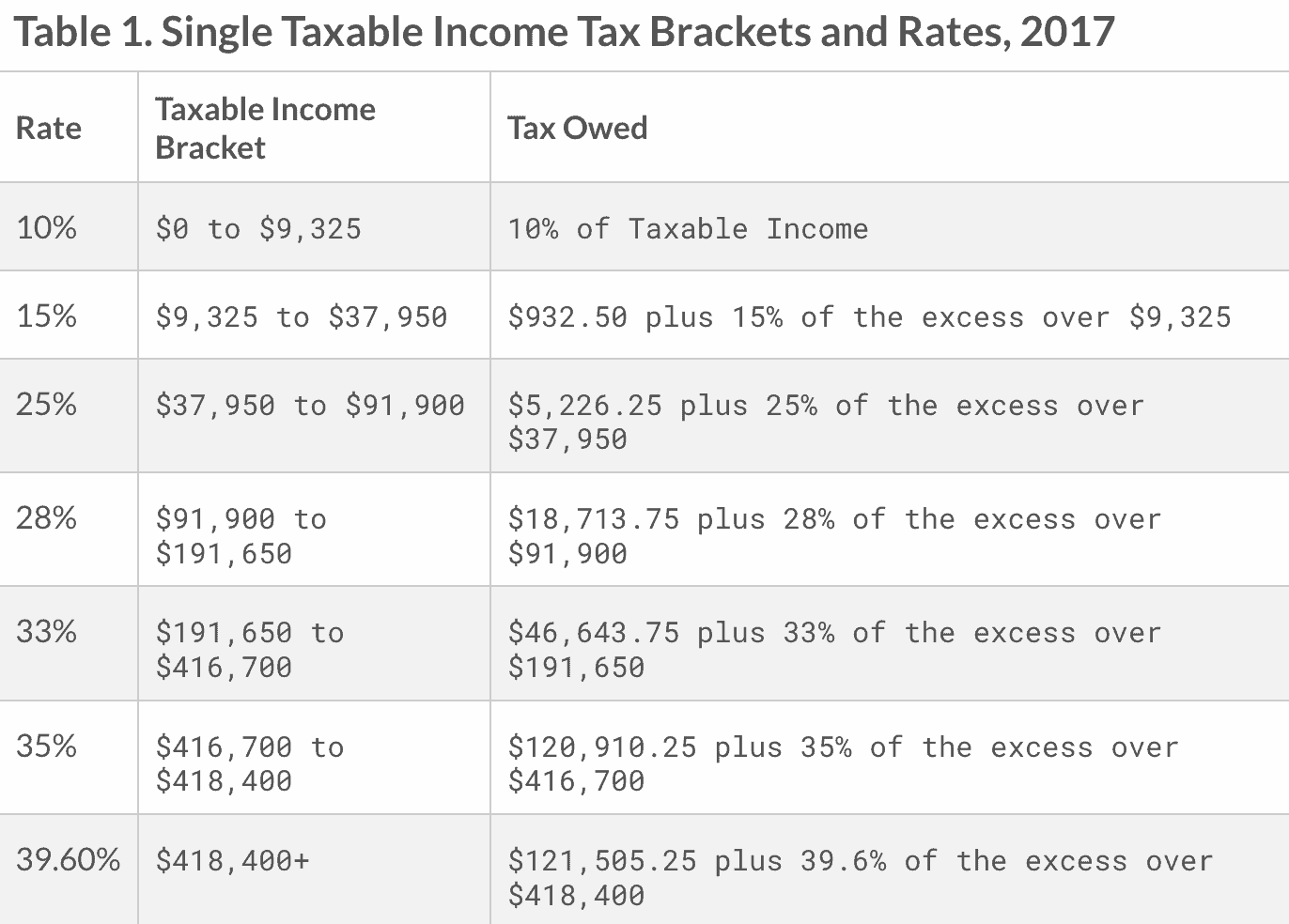

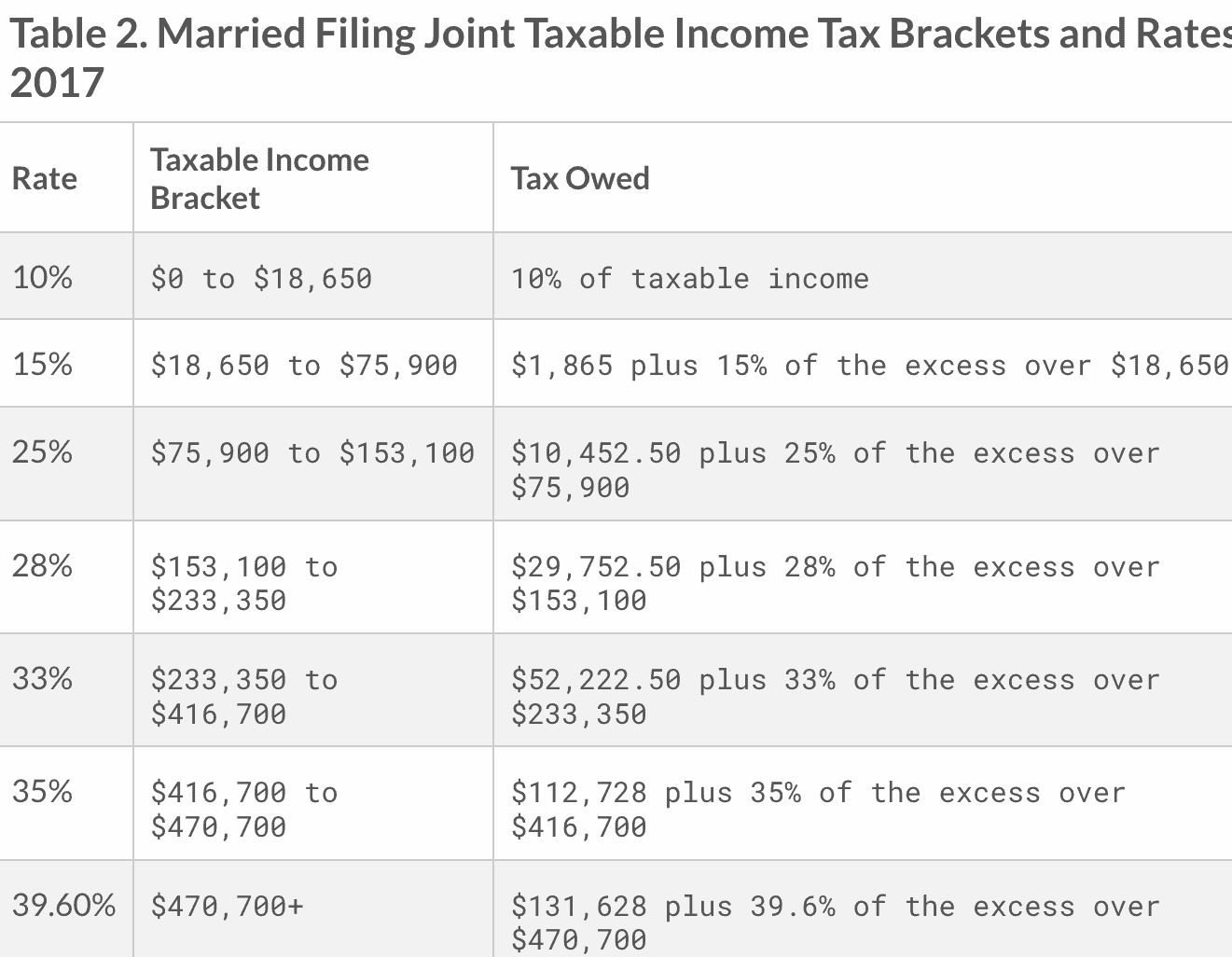

Now, let’s review the tax brackets from 2017 in Figures 2 and 3 to see what we can expect in 2026.

FIGURE 2 – 2017 Tax Brackets for Single Filers – Tax Foundation

FIGURE 3 – 2017 Tax Brackets for Married Filing Jointly – Tax Foundation

Why It Makes Sense to Consider Roth Conversions with Tax Rates Sunsetting in 2026

Hopefully, those numbers can help illustrate the importance of taking advantage of the current (lower) tax rates. You might have noticed that we’ve discussed Roth conversions quite a bit in a lot of our recent content. They were No. 1 on our list of 8 Ways to Prepare for a Recession earlier this summer (and you probably know by now that we’re technically in a recession).

Going to higher tax brackets just makes the tax-free income from Roth conversions that much more appealing. Remember that the Roth money can’t be taken out penalty free for the first five years after initial funding, regardless of your age. Once this five-year period is met, you can access principal of the Roth account even if you have not yet reached age 59½. If all your principal is distributed before age 59½, any earnings distributed from the account are subject to a 10% early withdrawal penalty. There are additional rules as well, so make sure you always consult your CFP® professional before withdrawing funds from your Roth account to avoid unintended taxes and penalties.

Looking at Various Tax Planning Strategies

Our CFP® professionals work closely with our in-house CPAs to look over financial plans from a tax planning perspective. Roth conversions are just one example of tax planning strategies. You can learn more about those by reviewing our Tax Reductions Strategies Guide. This guide explores various strategies for how to pay as little tax as possible over your lifetime. So, check it out below.

Download: Tax Reduction Strategies Guide

Obviously, 2026 is less than five years from now. So, if you’re 54½ or younger, the sooner you start your five-year clock on Roth conversions, the better. And to sum it all up with Roth conversions, by converting now while we have lower tax rates, you’re paying a lower tax when doing that conversion. So, why not take advantage of that discount?

How Do Tax Rates Sunsetting in 2026 Impact Capital Gains?

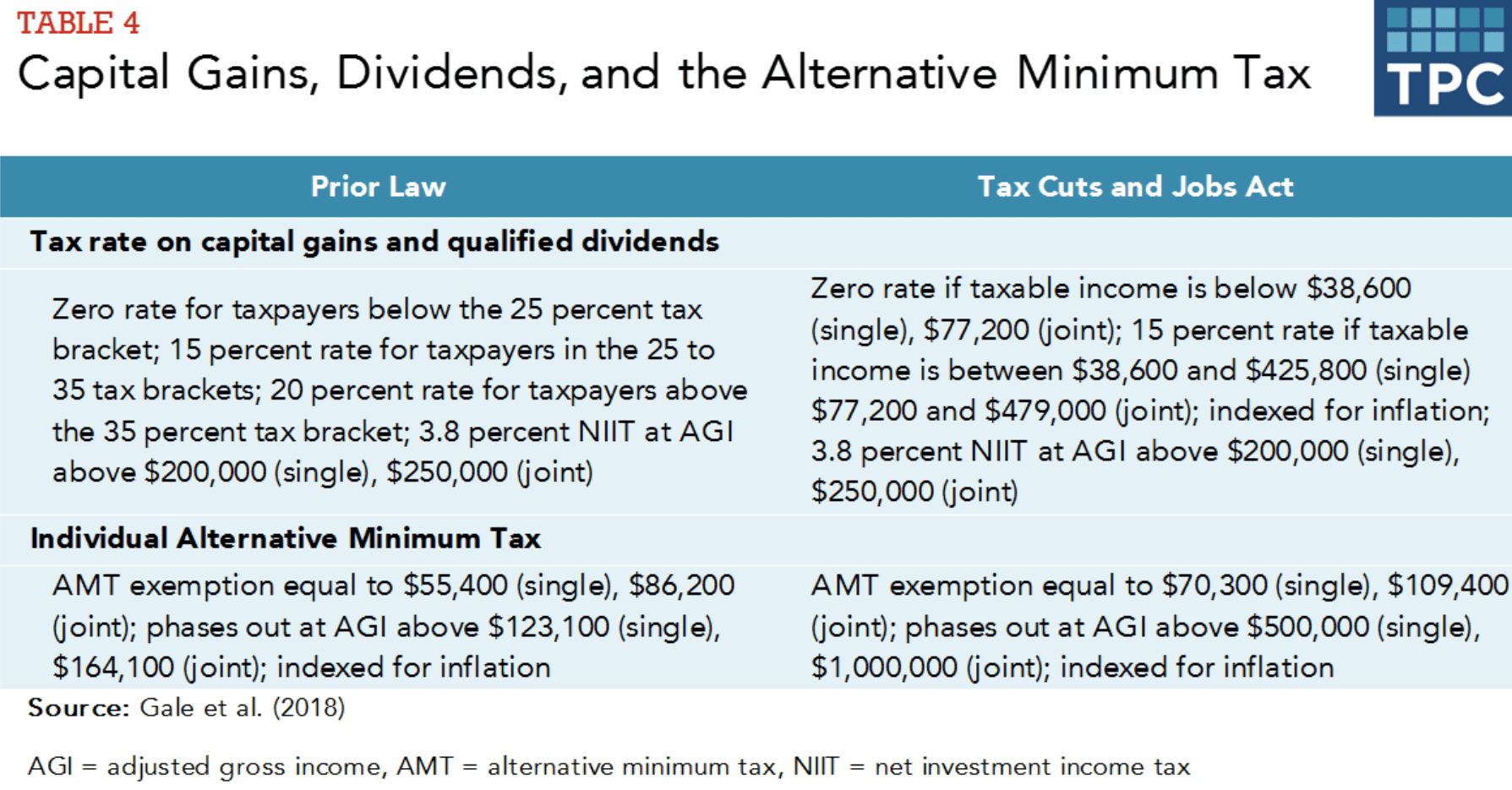

Again, as we look ahead to tax rates sunsetting in 2026, we must look back to 2017 to assess the legislation that was in place prior to the TCJA. The passing of the TCJA included notable changes in capital gains, the estate tax, and standard and itemized deductions. Let’s shift our focus next to Figure 4 to see the impact that the TCJA has had on capital gains, dividends, and the Alternative Minimum Tax.

FIGURE 4 – Capital Gains, Dividends, and the Alternative Minimum Tax – Tax Policy Center

So, there are some aspects of capital gains that are staying the same after tax rates sunset in 2026. But there are some changes that we don’t want to overlook as well. The preferential tax rates on long-term capital gains and qualified dividends remained unchanged after the TCJA went into effect in 2018. Therefore, they’ll remain unchanged after the tax rates sunset in 2026 as well. The same goes for the 3.8% net investment income tax that’s in place. There is a lot that goes into the NIIT: dividends, capital gains (short-and long-term), passive business income, and rents and royalties.

Now, that’s get to what changed about capital gains and dividends because of the TCJA. According to Tax Policy Center, “(The) TCJA separated the tax-rate thresholds for capital gains and dividend income from the tax brackets for ordinary income for taxpayers with higher incomes.” That separation will be no more come 2026.

The Individual Alternative Minimum Tax Thresholds Will Be Increasing Back to 2017 Levels

In terms of the Individual Alternative Minimum Tax, it remained after the TCJA was passed. However, the exemption levels were increased as well as the income threshold for the phasing out of the AMT exemption. That, in turn, drastically cut down the number of taxpayers impacted by the AMT due to the TCJA. If you believe you will be subject to the AMT exemption after these tax rates sunset in 2026, reach out to a tax professional about what your best plan of action might be. And, remember that the phaseout thresholds and exemptions totals will continue to be indexed for inflation.

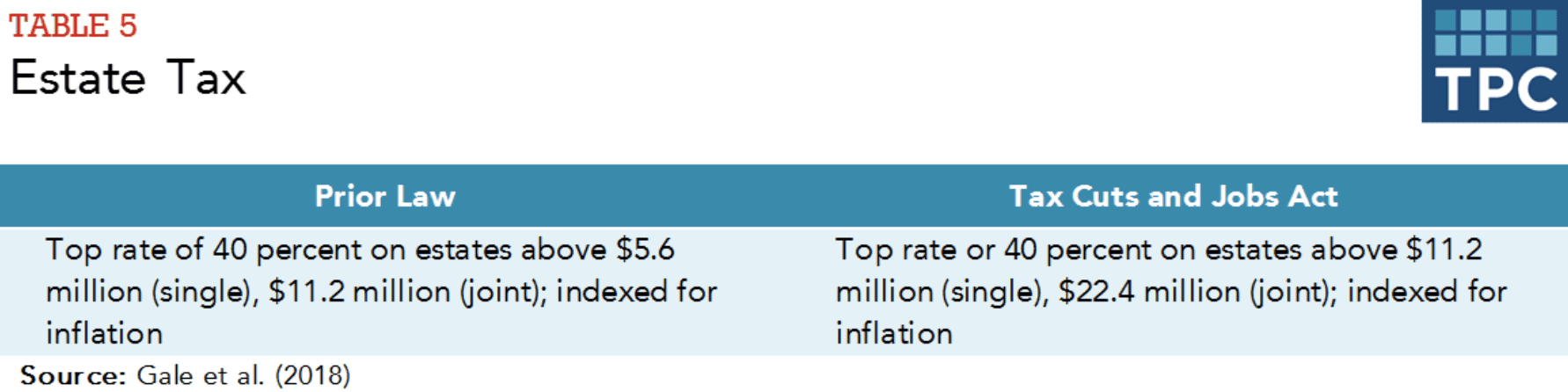

Significant Changes Regarding Estate Tax

One of the biggest changes we’ll see with the tax rates sunsetting in 2026 involves the estate tax. Currently, the estate tax exemption is at $11.2 million for single filers and $22.4 million for married filing jointly. We’ll be going back to 2017’s estate tax exemption numbers, which were $5.6 million for single filers and $11.2 million for married filing jointly. Of course, indexing for inflation factors in here as well. One thing that will be unchanged regarding estate tax is that the top rate will stay at 40%.

FIGURE 5 – Estate Tax – Tax Policy Center

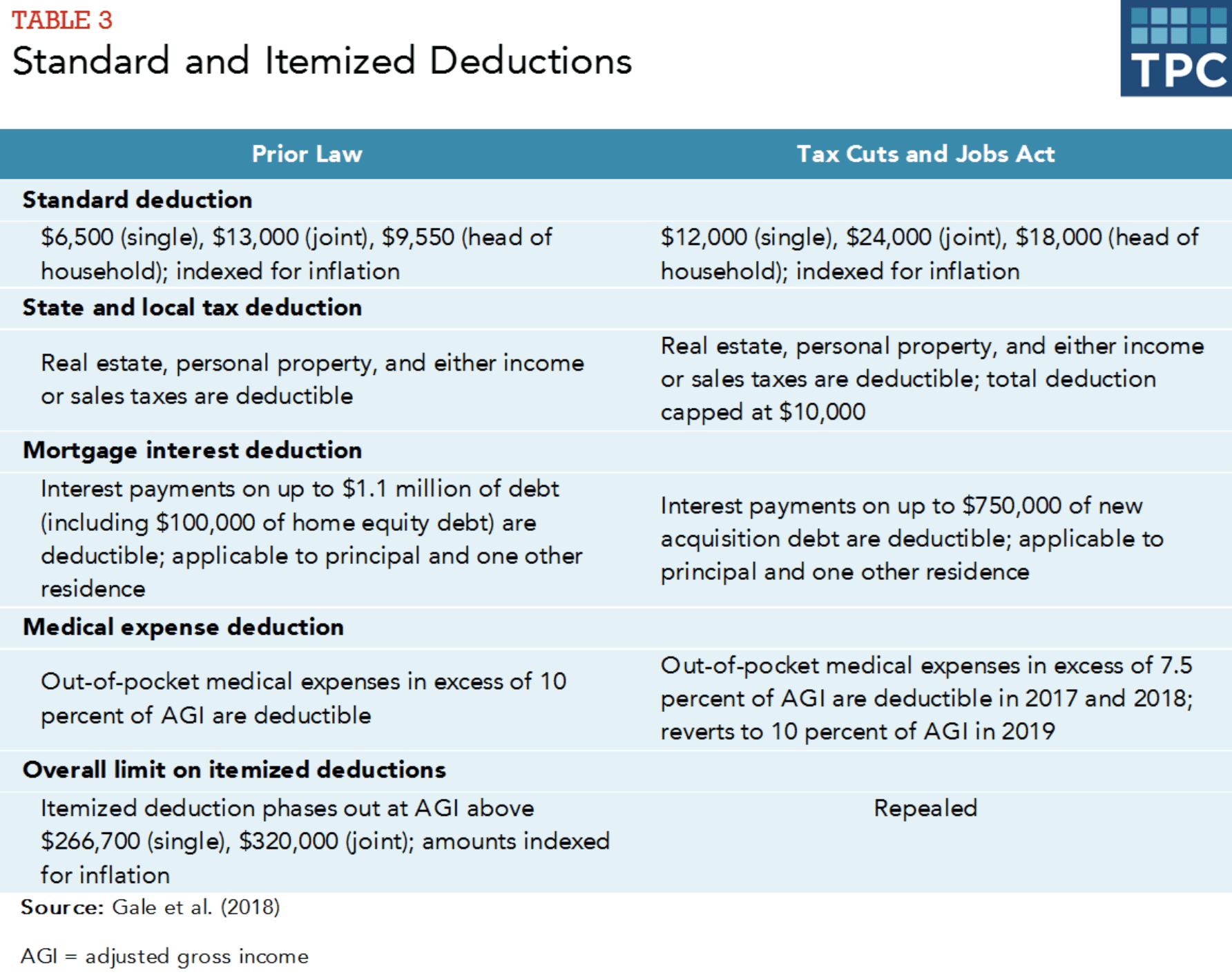

Changes to Prepare for with Standard and Itemized Deductions

OK, buckle up. There’s been a lot to take in so far on this ride of what to prepare for with the tax rates sunsetting in 2026. But there are a few more bumps in the road that we want you to be ready before the end of 2025. Many of them involve Standard and Itemized Deductions, as shown in Figure 6.

FIGURE 6 – Standard and Itemized Deductions – Tax Policy Center

Standard Deductions

Let’s start with the standard deduction amounts. Under the TCJA, standard deduction totals were nearly twice that of 2017’s numbers. So, prepare for significantly lower standard deductions these tax rates sunset in 2026. Not to beat a dead horse, but it’s critical to remember that standard deduction totals are indexed for inflation too. The lower standard deductions figures to drastically increase the number of taxpayers who want to itemize their deductions.

Itemized Deductions

Speaking of itemized deductions, their structure was altered quite a bit due to the TCJA. According to the Tax Policy Center, “Under prior law, itemizers could claim deductions for all state and local property taxes and the greater of income or sales taxes (subject to overall limits on itemized deductions).” So, that’s something to keep in mind once we return to pre-TCJA legislation in 2026.

The TCJA has restricted itemized deduction for total state and local taxes to $10,000 per year. That has applied for single and married filing jointly. That $10,000 cap will go away, though, after 2025. One thing that will remain constant is that taxpayers won’t be able to claim a deduction for state and local taxes against the AMT.

One last note on itemized deductions. The TCJA revoked the phase-down of the number of allowable itemized deductions. This has been referred to as the Pease provision. Starting in 2026, though, we’ll go back to having limitations for those with average gross income higher than $266,700 for single filers and $320,000 for those who are married filing jointly.

Other Deductions

There are a few more deductions we want to highlight before wrapping up this article on tax rates sunsetting in 2026. Before the TCJA, taxpayers were allowed to deduct interest on mortgage payments associated with the first $1 million of principal paid on debt incurred to purchase a primary and secondary residence plus the first $100,000 in home equity debt. That applied for significant renovations as well.

Taxpayers who have started new mortgages since 2018 have had the deductibility restricted to the interest on the initial $750,000 of loan principal and cut the deductibility of interest for home equity debt. That all ends after 2025, so act accordingly while preparing to return to pre-TCJA legislation.

Prior to the TCJA passing, taxpayers were also able to deduct out-of-pocket medical costs above 10% of adjusted gross income. That included health insurance costs. The TCJA reduces that from 10% to the current percentage of 7.5%. So, we’ll be going back to 10% in 2026.

Paying the Least Amount of Taxes Over Your Lifetime

These are just a few main takeaways in terms of why the current tax rates sunsetting in 2026 matters. With tax rates going up after 2025, we want to make sure that you’re doing everything in your power to pay the least possible amount in taxes. That’s not only now and in the next few years leading up to 2026, but over your lifetime.

Doing forward-looking tax planning is a big piece of the puzzle to the biggest question we often hear from pre-retirees. That question is: How Much Do I Need to Retire? It’s not easy to keep up with everything that’s going on in the tax code. We hope that you can get a better understanding of your current and future tax situation by using our financial planning tool that we mentioned earlier. Click the “Start Planning” button below to take control of your tax situation and live your one best financial life.

We’re Here to Answer Your Questions

While using our financial planning tool, it is very important to remember that it’s intended for professional use. That’s where we’re more than happy to help answer any questions you may have about the tax rates sunsetting in 2026 or any components of financial planning. Simply click here to schedule a 20-minute “ask anything” session or complimentary consultation with one of our CERTIFIED FINANCIAL PLANNER™ professionals. They can screen share with you while you’re using our financial planning tool so you can build your plan at your own pace and get the clarity and confidence that’s critical to getting to and through retirement.

Schedule a Complimentary Consultation

Click below to get started. We can meet in-person, by virtual meeting, or by phone. Then it’s just two simple steps to schedule a time for your Complimentary Consultation.

Investment advisory services offered through Modern Wealth Management, LLC, an SEC Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management an SEC Registered Investment Adviser. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.